Tags

- Buybacks are a direct and natural response to the shift in corporate management structure in the late 1970s which ushered in the period of ‘shareholder primacy’. It was Rule 10B-18 in 1982 which legitimized them.

- Banning share buybacks without also changing the focus away from maximizing shareholder value will accomplish little because companies will simply find other ways to reach that objective.

- The 1970s were a tumultuous period for the global economy with the two oil crises leading to stagflation and to enormous pressure on corporate profits. But the ground was set already in 1970 when M. Friedman published “The Social Responsibility of Business is to Increase Profits”.

- In 1976 M. Jensen & W. Meckling published “Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure” which explored the idea of equity-based compensation for professional managers.

- Finally, six years later Rule 10B-18 provided safe haven for companies to buyback their shares, allowing them another option to reward shareholders, in addition to dividends. The results were explosive.

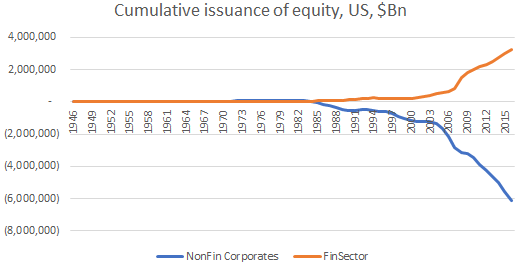

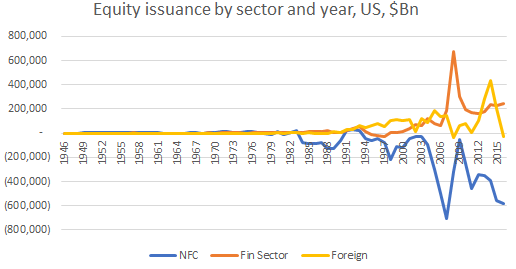

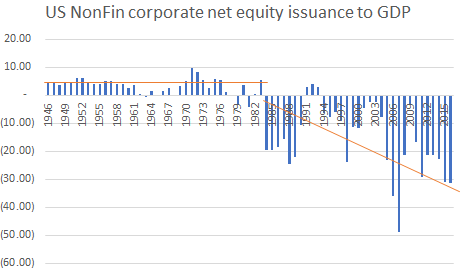

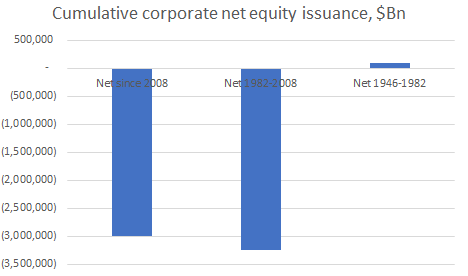

- Equity-based compensation rose from 0% of the median executive’s pay in 1980s to at least 60% in the 2000s; just in 1983, the aggregate amount of cash spent on share buybacks tripled and by 1985 it was 5 times higher than the average in the period 1972-1982.

- With the incentive structure thus created in the 1980s, companies NOT doing buybacks would not be fulfilling their objective of maximizing shareholder value, notwithstanding that managers are also large shareholders.

- Thus, banning buybacks makes no sense as it goes against the shareholder primacy doctrine unless, of course there is solid evidence that buybacks erode long-term shareholder value. So, therefore, the issue is not with buybacks but with the corporate management structure which has emerged since the 1980s.

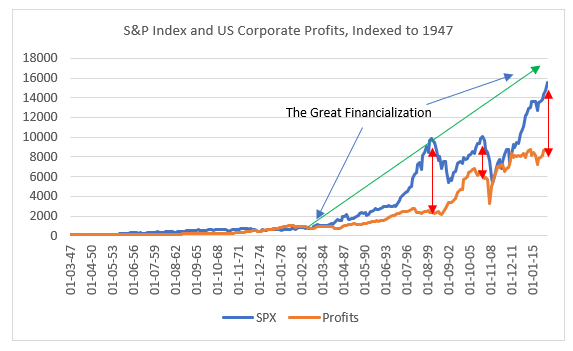

- Profit maximization and focus on shareholders has created extremely efficient companies boosting aggregate supply(AS), in many cases at the expense of aggregate demand(AD) at home, thus forcing those same companies to shift sales increasingly abroad.

- It has also contributed to the concentration of both companies and shareholders, the former leading to the monopolization of US industries, the latter to US inequality->continuing with the shareholder primacy thus could indeed be damaging to corporate profits long terms once AD dries off even in EM.

- I think it is difficult if not impossible to gauge the size of the effect of share buybacks on stocks prices or EPS, but there is no doubt that there is one: JPM, for ex. thinks effect on EPS growth is less than 10%, UBS thinks it is more than 30%.

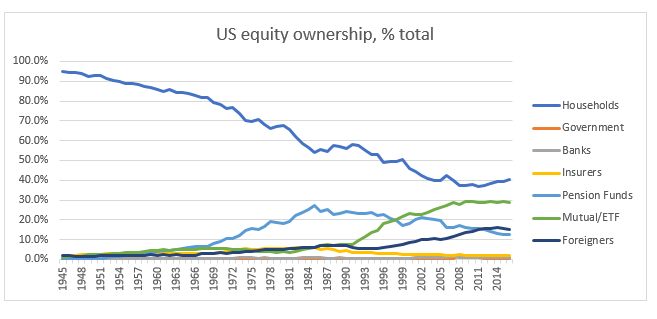

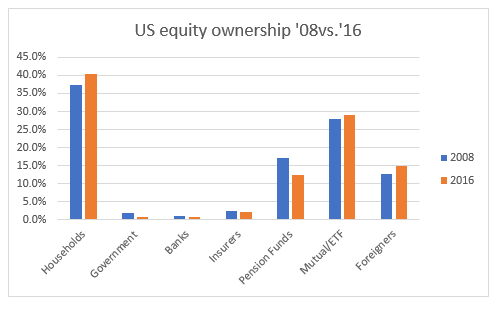

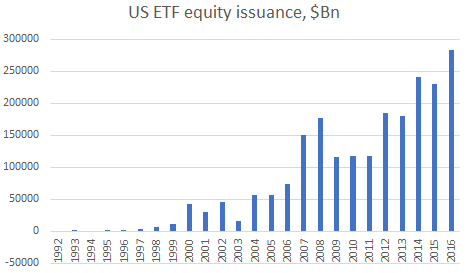

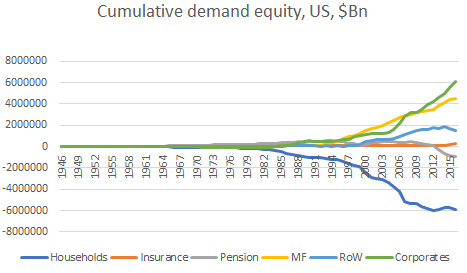

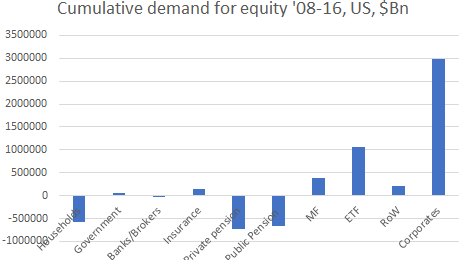

- Fed’s Z1 Flow of Funds reports a break-down of the major equity buyers each quarter: since 2008 corporates buying back their shares is absolutely dominant; the second biggest ‘buyer’, ETF, is three times smaller; pension funds and households net sold equities during that period.

- The stock price of profitable companies like Apple should be rising on its own merit , but that does not negate the possibility that buybacks ‘juice up’ stock prices even higher than ‘justified’. It goes the other way too: with 22 consecutive quarters of declining revenues the stock price of IBM probably should be lower -where would IBM stock price be if not for buybacks?

- If we are adjusting R&D to GDP, we might as well adjust share repurchases to GDP as well (and yes, they are also at record high). Tech companies raising their R&D – that’s great – but if they did not do any buybacks, could they have raised it even more?

- The recapitalization argument (shifting from equity to debt refinancing) is probably the most logical argument in favor of buybacks, if it was not for the agency conflict of interest (managers are equity holders) and the fact that they could have also boosted dividends instead.

- The argument that giving money back to shareholders could boost wages and investment somewhere else (therefore, where is the problem?) – yes, it could – but as far as I am aware there is not much evidence of this.