Tags

So, I have been doing a bit more work on trying to quantify US fiscal response to Covid-19 on US household income, consumption, savings and the stock market. Most of the data, I have been using, is from BEA Table 2.6; some is from the BLS employment/compensation report. The complete data set is only updated to July, unfortunately, but I have done projections for August and September where necessary. We will get the new data set on October 1, in a few days.

Bottom line is that without a new fiscal deal, US households will start digging into accumulated substantial savings to cover losses from unemployment which will prop up consumption but, most likely, expose the stock market to the downside.

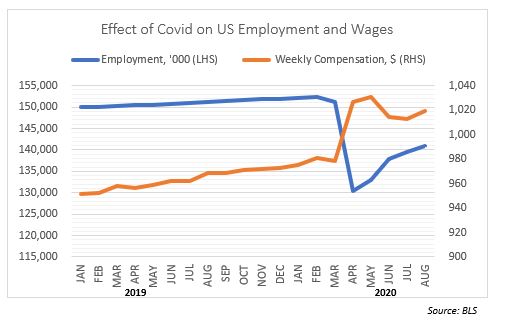

We all know that Covid-19 produced an employment shock comparable only to the Great Depression: there are still some 11.5m fewer people, or so, not employed vs to pre-Covid. The surprise (to me) was the fact that there was a 4.5% jump in weekly compensation, MoM, from February to August this year. This, on its own, cushioned a bit the overall purchasing power of the private sector.

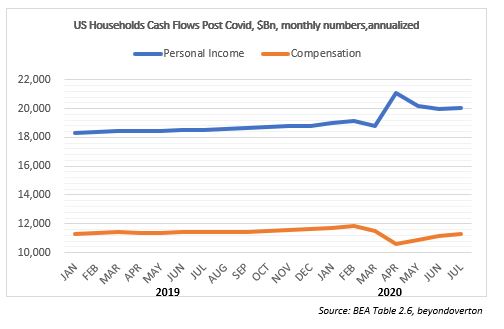

As you can see, actually, personal income did rise immediately after Covid, and is still some 5% higher from February this year. However, for sure it was not due to a rise in employment compensation (# people employed x wage rate,) despite the rise in weekly wages (see previous chart). In fact, overall compensation is still down almost 5% from February.

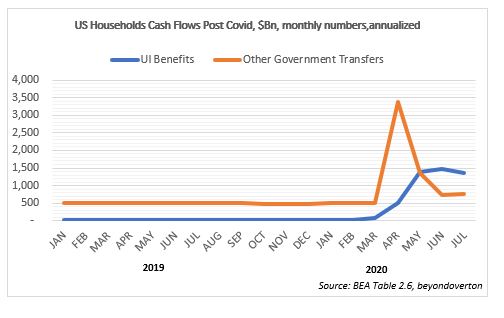

The reason HH income rose, was active fiscal policy which substantially increased UI Benefit and other government transfers post Covid. The annualized numbers exaggerate a bit this, but, nevertheless, the size of the increase is beyond anything previously done and also more than offsets the decline in employment compensation (see further down).

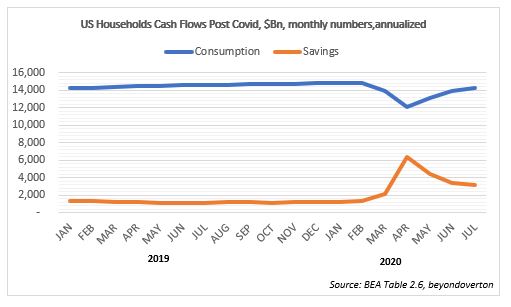

So, what did HHs do with the extra money? Well, they did not spend them: consumption is still down about 5% from February. HHs’ savings, on the other hand, rose substantially in the meantime.

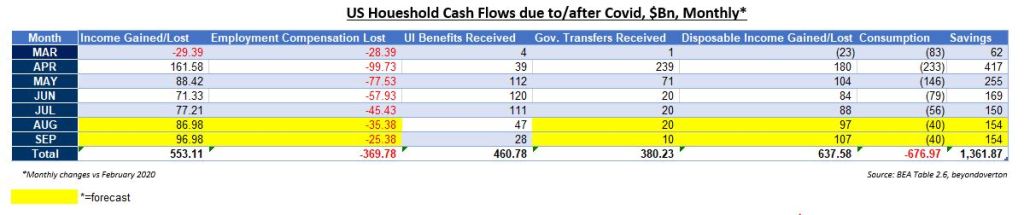

The table below breaks HHs’ cash flows net of their level from before Covid, and it is also on a monthly basis, so it is easier to see how the lost income from unemployment is more than offset by the unemployment insurance benefit payments. Then, on top of that, we’ve had further government transfer payments as part of CARES Act. No wonder the savings rate is so high!

Here is a snapshot of the same table netting off just the employment vs the benefits/transfer flows. US HHs had a negative cashflow only in March. Since then, they have net received income despite the high unemployment rate. Even in August and September, the loss income was more than offset with UI Benefits (not sure how that is possible as the UI payments stopped in July but that is what the data shows).

But both the UI payments and the government transfers are winding down. In October, US HHs might just about break even as employment compensation might not jump up to offset them.

The good news is that HHs have a very large cushion of savings on which to draw on, an extra $1.4Tn (this number also cross-references with Fed H.8 report on bank deposits). So, if anything, the economy would probably be fine. The bad news is that, to an extent that those savings were invested in the stock market, asset prices might find it difficult to rally.

So, there are two conclusions to be made. First, the extent of the fiscal support to the stock market in the past five months is not to be underestimated: if anecdotal evidence and data from retail brokerages are taken together, a big chunk of the households savings was invested in stocks. The fact that government assistance was still bigger than lost gains from unemployment in August (despite the expiry of some UI benefits in July) explains why the stock market remained bid throughout the month.

Second, the pressing need to pass the next phase of the fiscal stimulus is not to save the economy so much, but to save the stock market. Households have amassed about $1.4Tn of extra savings post Covid. As government assistance cannot cover the lost gains from unemployment going forward, without a new fiscal stimulus, some of that savings will most likely be re-directed from stocks to consumption leaving the stock market exposed to the downside.