Tags

This is my reading of an excellent paper by S&P Global, “Examining Share Repurchasing and the S&P Buyback Indices in the U.S. Market” by Liyu Zeng and Priscilla Luk, March 2020.

Over the past 20 years (up to end of 2019), the S&P 500 Buyback Index had outperformed the S&P 500 in 16 out of 20 years, or about 5.5% per year. YTD, it has underperformed, though, by about 14%! With that it, has managed to erase the last 10 years of outperformance!

We had similar underperformance of the buyback index in the early stages of the last financial crisis, in 2007; while in 2009, the S&P 500 Buyback Index had a significant excess return. Make your own conclusions where we are in this cycle.

Reality is that “buybacks tend to follow the economic cycle with increased or decreased repurchase activities in up or down markets while dividend payouts are normally more stable over time, the S&P 500 Dividend Yield portfolio tends to outperform in down markets, while the S&P 500 Buyback Index may capture more upside momentum during bull markets.“

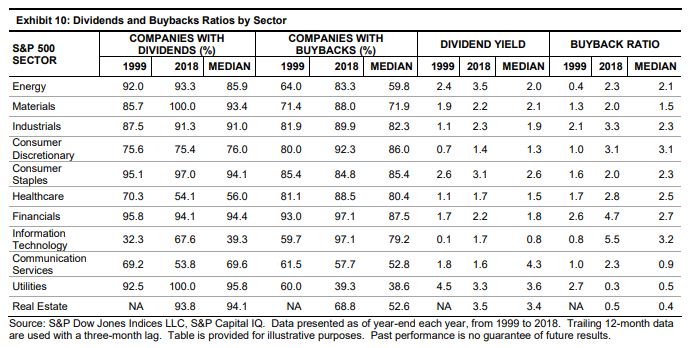

Almost all of tech, financial sector and consumer discretionary companies engage in share buybacks. Less than 50% of utilities do (but they all pay dividends). As share buybacks tend to congregate in cyclical rather than defensive sectors, the buyback index tends to underperform during recessions (this year).

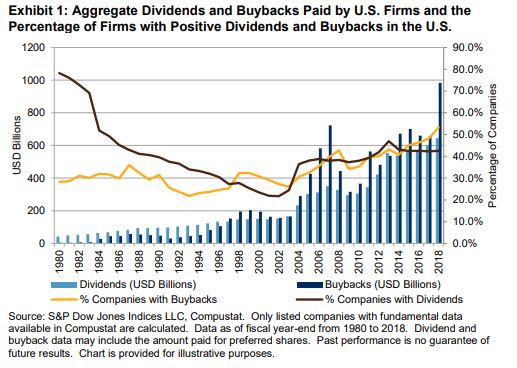

Since 1997, the total amount of buybacks has exceeded the cash dividends paid by U.S. firms. The proportion of dividend-paying companies decreased to 43% in 2018 from 78% in 1980, while the proportion of companies with share buybacks increased to 53% from 28%.

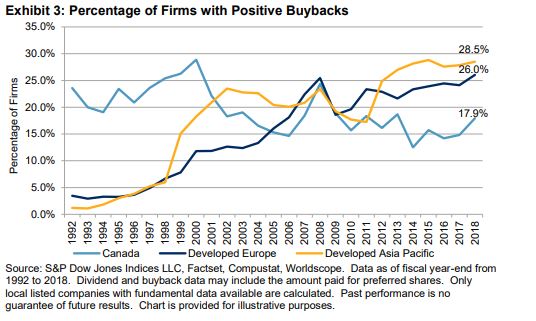

Compare to other developed markets. Despite an increase of share repurchases in Europe and Asia, as a % of all companies, buybacks still stand at about half that in the US. On the other hand, fewer Canadian companies engaged in share buybacks during that period.

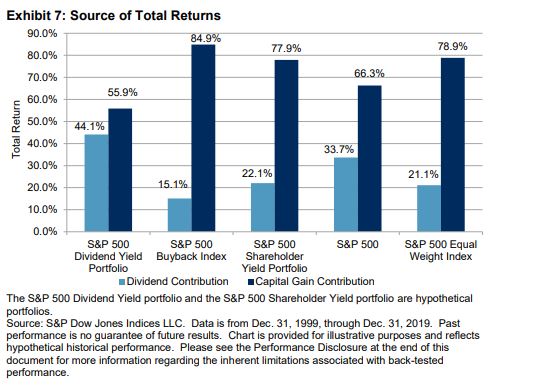

For the S&P 500 Index, over the last 20 years, 2/3 of the total return has come from capital gains and only 1/3 from dividends. Before the mid-1980s, when buybacks became dominant, the opposite was true. Buybacks have been instrumental in driving equity returns since the mid-1980s.