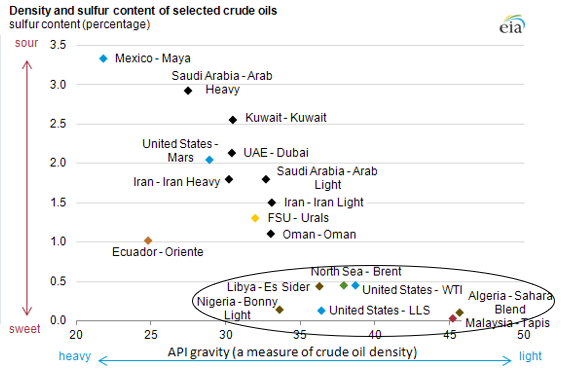

- Not all oil is ‘created equal’: US WTI and European Brent are light and sweet, most of OPEC is heavy and sour, Russia’s is kind of in the middle. These distinction matter not only because of the different qualities, but more importantly, because of whether the oil is refinery-ready.

Diagram 1

- Therefore, direct comparisons between OPEC and US Shale Oil, for example, is like comparing apples and oranges -> same category but very different at the same time. Instead, US Shale Oil’s direct competitors are the ones in the circle above (see also Chart 4, see below).

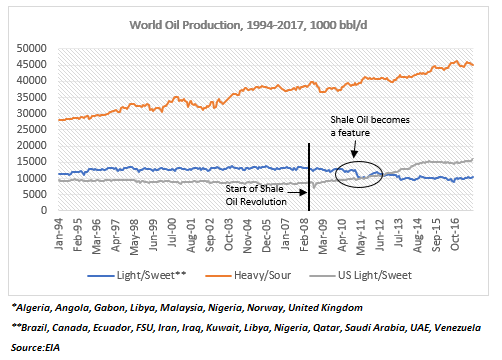

- If we grossly oversimplify and break world oil production into two categories: Light/Sweet are all US competitors (circled above), with API>35, and Heavy/Sour are mostly OPEC/Russia/Canada with API<35, as per above diagram, this is how it would look over time.

Chart 1

- US’ main oil competition started reducing production at about the same time the US shale revolution first geared its head above the horizon post the 2008 financial crisis; then, as US shale production really took off in 2011-12, the rest of global Light/Sweet production dutifully collapsed.

- Heavy/Sour Production is the dominant feature here, equal to 63% of total world oil production, vs 37% for Light/Sweet. However, it is off the peak reached in 2011 when US shale oil production really took off.

Chart 2

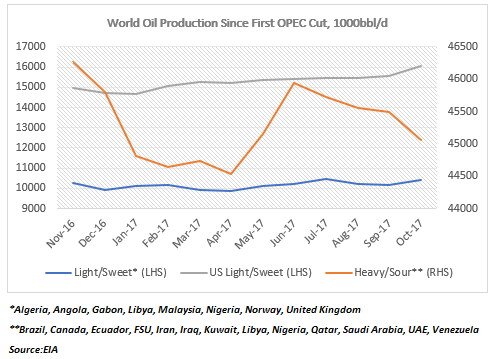

- The recent rise of Light/Sweet oil production relative to Heavy/Sour is a combination of both OPEC cuts since November 2016 and a continuous in increase in US Shale Oil production. However, the increase in US Shale Oil since the 2008 financial crisis is more or less offset by the decrease in rest of the world Light/Sweet production.

Chart 3

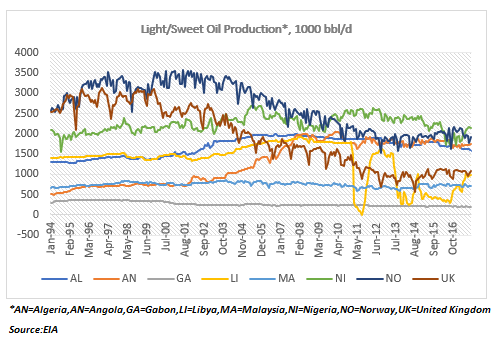

- In fact, Norway peaked in the early 2000s; Nigeria: in mid-2000s; UK in the mid-1990s; Algeria, Angola et all, all peaked towards the late 2000s. But the one that really stands out is Libya: before it collapsed in 2011, Libya was one of the largest Light/Sweet oil producers.

Chart 4

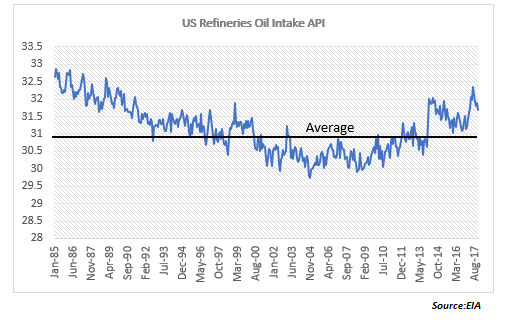

- Because US used to import a lot of heavy OPEC oil in the past, most of US refineries are suited to low API oils. In fact, the average API of oil that enters US refineries is about 31. This is lower than European refineries, used mostly to Brent, with API of around 36.

Chart 5

- The problem is this adjustment is far from easy. Only a very small portion of US oil is refinery-ready. And that proportion is decreasing as more lighter shale oil is produced year after year: majority of US production is now in the 40-45 API range; only 13% is refinery-good.

Chart 6

- So, US refineries need to keep importing more Heavy/Sour oil just so that they are able to refine the domestic shale oil. The other alternative is to export the crude shale oil directly to be refined abroad. But there are very few refineries even abroad that can accommodate Light/Sweet.

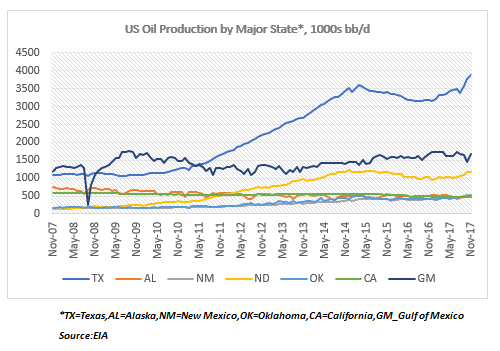

- Why is US oil getting lighter and lighter? Because of shale oil and specifically because of Texas: it is the largest producer of US oil, a title it took over from the Gulf of Mexico in 2011 when US shale oil production took off.

Chart 7

- And Texas oil production continues to rise thanks to the Permian Basin: Eagle Ford is off the peak and barely rising. In fact, the Permian Basin and the Gulf of Mexico are now the only two major oil producing regions in the US really growing.

Chart 8

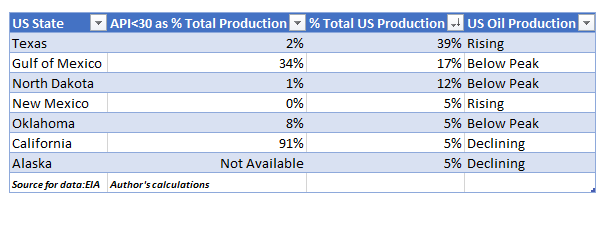

- The problem with Texas oil production rising is that only 2% of it is refinery-ready. In fact, of the three largest oil producing regions in the US, two are below their peaks, and only one, Gulf of Mexico, has a low enough API to be refinery ready.

Table 1

- New Mexico shale oil production is rising but none of it practically is refinery-ready; North Dakota and Oklahoma are below peak and only 1% and 8% of their oil, respectively, is refinery-ready; California and Alaska, which are producing more conventional oil, have been on a decline for a while.

Bottom line:

- US and OPEC are not really in competition because they produce completely different crude oils. Moreover, US refineries and a large number of other refineries around the world are more suited to OPEC oil than to US shale oil.

- US shale oil API is rising because the old shale oil wells are depleting much faster and the new ones, where the oil is even more difficult to reach, have a higher API->that will put further strain on US refineries (increased Heavy/Sour imports).

Chart 9

What happens when oil production in the Permian Basin also starts to decline?