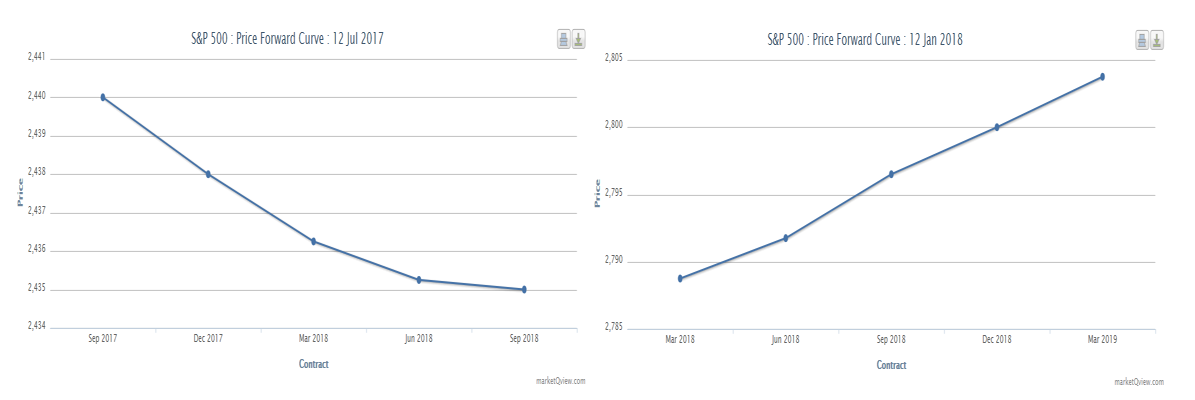

For the first time since 2009, the market gets ‘paid’ to be short US equites. With the S&P 500 Forward Futures curve moving from backwardation to contango, equity shorts start to earn positive carry. This may not mean an automatic reversal of the strong positive equity trend in US equities but it does remove one of the fundamental pillars of CTAs, momentum-driven and some algos in executing long S&P 500 Futures strategies.

1. Trend followers will tell you that the most powerful combination is when you are paid to be in the momentum. i.e. when you are not only riding the momentum but you are also getting paid to do that (you are earning positive carry).

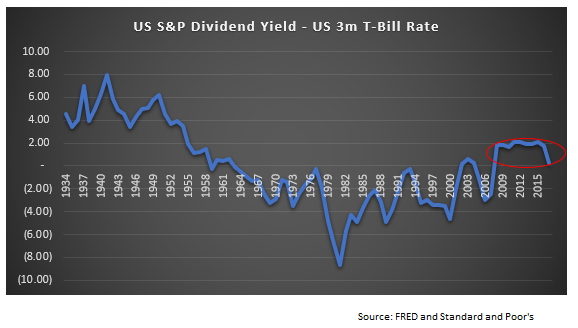

2. This is exactly what has happened in US equities since 2009: if you have been long US stocks through US index futures, this has been a positive carry trade in addition to being also a very powerful long-term momentum trend.

3. This is actually quite unusual: the dividend yield was lower than the 3m TBill rate between the late-1950s till 2008 and long stocks through futures (early 1980s) had been a negative carry trade. In fact, the negative carry was around 2.5% pa during that period.

4. Since 2008, however, the opposite has happened: with the dividend yield climbing above the 3m TBill rate, the carry of being long stocks through futures has flipped to an average of around +2% providing massive support to the stock market positive trend.

5. (When the dividend yield is lower than 3m TBill rate, the SPX futures curve is in contango, and is in backwardation in the alternative scenario).

6. Since last year, though, things have changed: with the Fed rising rates and the 3m Tbill yield moving up, the SPX futures curve first flattened out about 6 months ago and is now in contango.

7. With the Fed continuing to raise rates, the SPX futures forward curve is likely to continue to steepen (3mTBill 1y fwd went above SPX dividend yield last December) and thus the negative carry of long equities through futures will also start increasing.

8. Timing the market is a sucker’s game. People have been calling the end of the equity bull market the moment SPX reached the previous 2007 peak again in 2013. They have thrown everything at this call: valuations, flows, sentiment…

9. I have no idea if 2018 will be the year when this trend will break but being long equities has lost an important pillar of support: the carry. All of a sudden, for the first time since 2009, the market is ‘paid’ to be short SPX futures!