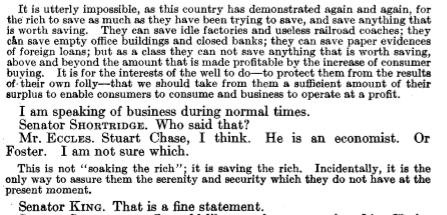

Marriner Eccles, Chair of the Federal Reserve, 1934-1948, one of the unsung heroes of the Great Depression in the US.

Below is from a Hearing before the Committee on Finance US Senate, February 1933.

- Before effective action can be taken to stop the devastating effects of the depression, it must be recognized that the breakdown of our present economic system is due to the failure of our political and financial leadership to intelligently deal with the money problem. In the real world there is no cause nor reason for the unemployment with its resultant destitution and suffering of fully one-third of our entire population. We have all and more of the material wealth which we had at the peak of our prosperity in the year 1929. Our people need and want everything which our abundant facilities and resources are able to provide for them.

- The problem of production has been solved, and we need no further capital accumulation for the present, which could only be utilized in further increasing our productive facilities or extending further foreign credits. We have a complete economic plant able to supply a superabundance of not only all of the necessities of our people, but the comforts and luxuries as well.

- Our problem, then, becomes one purely of distribution. This can only be brought about by providing purchasing power sufficiently adequate to enable the people to obtain the consumption goods which we, as a nation, are able to produce. The economic system can serve no other purpose and expect to survive.

- If our problem is then the result of the failure of our money system to properly function, which to-day is generally recognized, we then must turn to the consideration of the necessary corrective measures to be brought about in that field; otherwise, we can only expect to sink deeper in our dilemma and distress, with possible revolution, with social disintegration, with the world in ruins, the network of its financial obligations in shreds, with the very basis of law and order shattered. Under such a condition nothing but a primitive society is possible.

- The nineteenth century economics will no longer serve our purpose— an economic age 150 years old has come to an end. The orthodox capitalistic system of uncontrolled individualism, with its free competition, will no longer serve our purpose. We must think in terms of the scientific, technological, interdependent machine age, which can only survive and function under a modified capitalistic system controlled and regulated from the top by government.

- Money has no utility or economic value except to serve as a medium of exchange.

- The debt structure has obtained its present astronomical proportions due to an unbalanced distribution of wealth production as measured in buying power during our years of prosperity. Too much of the product of labor was diverted into capital goods, and as a result what seemed to be our prosperity was maintained on a basis of abnormal credit both at home and abroad.

- This naturally reduced the demand for goods of all kinds, bringing about what appeared to be overproduction, but what in reality was underconsumption measured in terms of the real world and not the money world.

- Why was it that during the war when there was no depression we did not insist upon balancing the Budget by sufficient taxation of our surplus income instead of using Government credit to the extent of $27,000,000,000? Why was it that we heard nothing of the necessity of balancing the Federal Budget in order to maintain the Government credit when we had a deficit of $9,000,000,000 in 1918 and $13,000,000,000 in 1919? Why was it that there was no unemployment at that time and an insufficient amount of money as a medium of exchange?

- Why resort to inflation of the sort referred to when prices can be increased and business revived on the basis of our present money system? We have nearly one and a half billion currency more in circulation at the present time than we had at the peak of 1929, and under our present money system we are able to increase this by several billion more without resorting to any of the three inflationary measures popularly advocated. There is sufficient money available in our present system to adequately adjust our present price structure. Our price structure depends more upon the velocity of money than it does upon the volume.

- I repeat there is plenty of money to-day to bring about a restoration of prices, but the chief trouble is that it is in the wrong place; it is concentrated in the larger financial centers of the country, the creditor sections, leaving a great portion of the back country, or the debtor sections, drained dry and making it appear that there is a great shortage of money and that it is, therefore, necessary for the Government to print more. This maldistribution of our money supply is the result of the relationship between debtor and creditor sections— just the same as the relation between this as a creditor nation and another nation as a debtor nation—and the development of our industries into vast systems concentrated in the larger centers.

- Senator WALSH of Massachusetts. When do you think prosperity will come back? Mr. ECCLES. It depends entirely on what the Government does. It will not come back unless action is taken by the Federal Government, in my judgment.

Note: Italics and bold are mine