“So, you think we might have put a few people out of business today. That it’s all for naught. You’ve been doing that every day for almost forty years Sam. And if this is all for naught then so is everything out there. It’s just money; it’s made up. Pieces of paper with pictures on it so we don’t have to kill each other just to get something to eat. It’s not wrong. And it’s certainly no different today than it’s ever been. 1637, 1797, 1819, 37, 57, 84, 1901, 07, 29, 1937, 1974, 1987-Jesus, didn’t that fuck up me up good-92, 97, 2000 and whatever we want to call this. It’s all just the same thing over and over; we can’t help ourselves. And you and I can’t control it, or stop it, or even slow it. Or even ever-so-slightly alter it. We just react. And we make a lot money if we get it right. And we get left by the side of the side of the road if we get it wrong. And there have always been and there always will be the same percentage of winners and losers. Happy foxes and sad sacks. Fat cats and starving dogs in this world. Yeah, there may be more of us today than there’s ever been. But the percentages-they stay exactly the same.” John Tuld in Margin Call

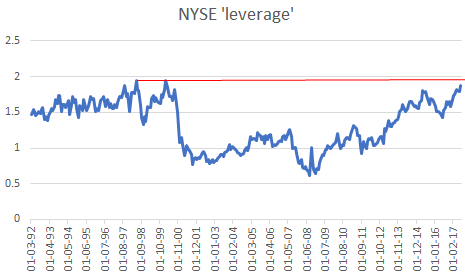

Source: NYSE. Leverage is calculated as the following ratio: NYSE firms debit balances in margin accounts (or margin debt)/ (NYSE free credit balances in cash accounts + credit balances in margin accounts)

Are stocks overvalued? This is the longest stock bull market without a X% drop since XXXX (input your own numbers; they are meaningless, anyway)… Sure, you must know your history and you must know your valuations. That’s the minimum when it comes to investing money. But none of them provides an edge. History is a pattern recognition puzzle, and, nowadays, as long as you provide the right inputs, even a simple algo would be able to sort it out. Valuation, on the hand, is just simple math. But again, you need the right variables. Knowing what to include and what to omit is tough but it is what would make a difference.

There is one thing, however, which I think beats all other ‘basic’ variables when it comes to figuring out the turning points in investment trends. I think that is leverage. Leverage matters especially in situations like we have today with stocks hitting all time highs and smart people questioning the sustainability of this long bull market. The thing is, we believe history and valuations provide the answers but it is a mind trick – we get the impression they do because that’s what we have been told and because it looks like this… but only in hindsight.

The market, however, can go down on anything that scares people if leverage is high. And it would not be one particular thing: everyone might have a different reason to sell. It could be a geo political event or it could be even something personal. But the underlying reason for selling would be the same – they had to sell!

“Everything needs to change, so that everything can stay the same” (‘Il Gattopardo’, Guiseppe Tomasi di Lampedusa). In other words, what is the context? The same event that happened 50 years ago might provide a totally different outcome now. If it was otherwise and life was linear, investing would have been too easy and life would have been too boring.

For example, history ‘changed’ in 1982 when rule 10B-18 was introduced providing ‘safe haven’ for US companies to buy back their own shares. Corporate buybacks were almost non-existent before. After this rule came into place, US corporates became the biggest buyers of US shares. The result has been negative net-issuance of US shares since at least 2000. Let me repeat that, the net supply of US shares (IPOs, etc. minus buybacks, etc.) has been negative for the last 17 years or so. How many people are taking this into account when they do their valuation analysis?

On the other hand, given how much the composition of stock indices has changed throughout time, how relevant is it to look at a time-series of index-based valuation variables? Aren’t we comparing apples to oranges? Should US Steel, for example, trade at the same multiples as IBM, Apple, Amazon? I do not have answers to these questions. And even if I did, it would be irrelevant because what matters is what everyone else also thinks, and even if I knew what everyone else thinks, it would be still irrelevant because people do not always do the things they should be doing or thinking. But people always act when they do not have a choice.

When your broker calls you to post some extra margin, which you cannot do, you do not have a choice but to sell. But, don’t worry, this is not going to happen when stocks are hitting all-time highs. So, don’t get too excited about getting the top of the market even if you know what the leverage is. But knowing that the leverage is too high and that, maybe, just maybe, people do not have a choice, will help you sell AFTER the market has gone down 2%, 5%, 10%… Whatever that number is, whenever you think the ‘pain’ becomes unbearable. This is when the trend changes and the buy-on-dip guys get buried and it becomes sell-on-pops.

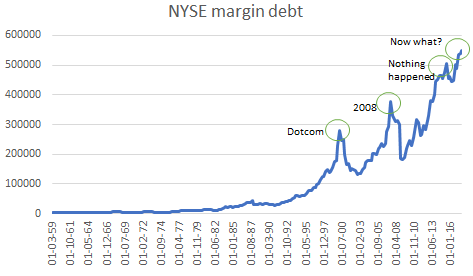

So, the trick is to measure the leverage or to at least to get an idea of how extended it is. One widely cited measure is the NYSE margin debt (the debit balances in margin accounts – chart below). I remember it was a compelling chart to look at in the summer of 2013 when margin debt was approaching the pre-2008 highs. But then it kept going and going, hitting new highs ever since… In the spring of 2015, after it had hit yet another high, it started dropping all the way until the beginning of 2016. And what happened to stocks? Nothing. Margin debt is sitting on a new high even now but anyone shorting stocks using this measure of leverage has not done that well recently.

Source: NYSE

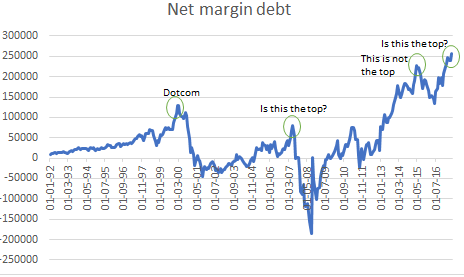

We can also look at the difference between the credit (+ cash) and debit balances of firms’ margin accounts on the NYSE. I call that net margin debt (chart below). That’s even more confusing as we can see the pre-2000 top but for some reason NYSE firms were in net credit (big negative spike) just before the Lehman Brothers bankruptcy. And again, since the summer of 2013 this measure of leverage has been hitting new highs.

Source: NYSE

Alternatively, we can look at the ratio between the two, or what I called, NYSE ‘Leverage’ (chart at the top of the post). This measure is approaching the highs reached at the peak of the Russia crisis and Dotcom crisis. Should we sell? How well would we have done if we followed this signal in 2008? Quite bad actually as this ratio hit the bottom the month before Lehman’s bankruptcy. But of course, 2008 was a ‘debt’ problem, not an ‘equity’ problem like 2000 was. Still US equities had a peak-to-trough decline of more than 50% back then. The bottom line is still that there was not much in the equity valuations and ‘nothing’ in equity accounts leverage that would have helped us predict such an outcome.

These charts above are not especially useful and would not have been much help in our investment decisions. That’s because even leverage has to be taken into context when looking at history. Because even if you have to post extra margin but you can still borrow at a reasonable rate (somewhere else) you might decide to choose the latter instead of selling. So, ceteris paribus, high leverage and high interest rates are the worst possible combination, but high leverage and low rates (the status quo since 2013 at least) means nothing.

Source: NYSE

Indeed, in the context of US interest rates, NYSE leverage actually looks reasonable, not too far from the lows post 2008 financial crisis (chart above). This is purely a function of how low rates have been in that period. Notice, for example, the high leverage throughout the 1990s when we also had a booming stock market. Which opens up another angle of thought. If rates do rise, as the base rate is indeed right now, then high leverage can quickly become a problem.