Tags

Despite the fanfare in the markets, the Federal Reserve’s monetary stimulus, on its own, is rather underwhelming compared to the equivalent during the 2008 financial crisis. What makes a difference this time, is the fiscal stimulus. The 2020 one is bigger than the 2008 one; but more importantly, it actually creates net financial assets for the private sector.

Monetary Stimulus

- Fed’s balance sheet has increased by 73% since the beginning of 2020. In comparison, it increased by 109% between August’08, the month before Lehman went bust and most major programs started, and March’09, the month when the stock market bottomed. Actually, by the time QE3 ended, in September 2014, Fed’s balance sheet had increased by 385% compared to since before the crisis.

- Commercial bank reserves were at 9% of their total assets before the Covid crisis and are sitting at 15% now, a 94% increase. In the aftermath of the 2008 crisis, on the other hand, bank reserves tripled from August’08 to March’09 and increased 10x by September’14. Relative to banks’ total assets, reserves were just at 3% before the crisis but rose to 20% by the end of QE3.

- Bank deposits were at 75% of their total assets in January’20 and are at 76% now, a 17% increase. Deposits were at 63% before the 2008 crisis, had declined to 60% by March’09, and eventually rose to 69% of banks total assets. Overall, for this full period, commercial bank deposits rose by 49%.

In percentage terms, Fed’s balance sheet rose less during the 2020 crisis than during the 2008 crisis and its aftermath.

Commercial bank reserves were a much smaller percentage of banks’ total assets before the 2008 crisis than before the 2020 crisis, but by the end of QE in 2014, they were bigger than today.

Banks started deleveraging post the 2008 financial crisis (deposits went up as a percentage of total assets) and continue to deleverage even now.

On the positive side, however, the Fed has introduced four new programs in 2020 that did not exist in 2008, Moreover, unlike 2008, they are directed at the non-financial corporate sector, i.e. much more targeted lending than during the financial crisis.

Nevertheless, very little overall has been used of the facilities currently, both in absolute terms (the new ones), and compared to 2008.

In fact, looking at the performance of financial assets, the market is not only telling us we are beyond the worst-case scenario, but, as equities and credit have hit all-time highs, it seems we are discounting a back-to-normal outcome already. It took the US equity market about four years after the 2008 crisis to reach its previous peak in 2007. In the 2020 crisis, it took two moths!

Following the 2020 Covid crisis, monetary policy so far is much less potent than following the 2008 financial crisis. Taking into account the full usage of Fed’s facilities announced in 2020, the growth rate in both Fed’s balance sheet and commercial bank reserves by the end of 2020 will likely match those for the period Auguts’08-March’09. But it has a long way to go to resemble the strength of monetary policy during QE1,2.3. Given that US equities only managed to bottom out by March’09, in an environment of much stronger monetary policy on the margin than today, means that their extraordinary recovery during the Covid crisis has probably borrowed a lot from the future.

Fiscal Stimulus

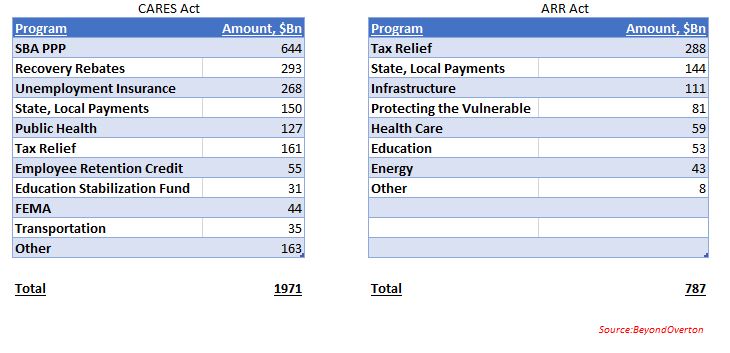

The Coronavirus Aid, Relief, and Economic Security (CARES) Act of 2020 is much bigger than the American Recovery and Reinvestment (ARR) Act of 2008, both in absolute terms and in percentage of GDP.

However, what really makes the difference, is the fact that the CARES Act has the provision to increase the private sector’s net assets. This is done through two of the programs. The SBA PPP allows for about $642Bn of loans to small businesses. If eligibility criteria are met, the loans can be forgiven. The Recovery Rebates Program allows for the disbursement of $1,200pp ($2,400 per joint filers plus $500 per dependent child). Nothing like this existed during the 2008 financial crisis.

Most of the loans through the SBA PPP have already been made, and about $112Bn are forgiven. So, there is another maximum of $532Bn which could still be forgiven (deadline is end of 2020). The Employment Rebate Programs is about $300Bn in size.

Just the size of these two programs can potentially be as big as the ARR Act was, in absolute terms. They create the possibility for the private sector to formally receive ‘income’, even though it is a one-off at the moment, without incurring a liability. Some of the other programs, like Tax Relief, are a version of that, but instead of acquiring an asset, the private sector receives a liability reduction – not exactly the same thing.

This is important. Until now, the private sector could receive income either in exchange for work, or, as it became increasingly more common starting in the late 1990s, with the promise of paying it back (in the form of debt). This now could be changing.

The Fed, for example, can not do that. Its mandate prevents it to ‘spend’ and only to ‘lend’. Until 2020, the Fed’s programs were essentially an exercise of liquidity transformation and a duration switch (the private sector reduced duration – mostly UST, MBS – and increased liquidity – T-Bills and bank reserves). There was no change in net assets on its balance sheet; the change was only in the composition of assets. The more recent programs introduced direct lending to the non-financial sector, still no net creation of financial assets, but a much broader access to the real economy.

In a sense, while the CARES Act comes closer to the concept of Helicopter Money or Universal Basic Income (UBI), the monetary stimulus of 2020 is moving closer to the concept of Modern Monetary Theory (MMT).

In that sense, while the reaction of financial markets to the monetary stimulus may not be deemed warranted, taking into account the innovative structure of the fiscal stimulus, asset prices overreaction becomes easier to understand. Still, I believe the market has discounted way too much into the future.

There is always a dichotomy between financial markets and the economy but, it seems that currently, the gap is quite stark between the two. It could be that the market is comfortable with the idea that, in a worst-case scenario, the authorities have plenty of ammunition to use, in the case of both the existing facilities as well as new stimulus.

I have been in the past quite critical of the prospect of fiscal policy to save the day. Regardless of how financial markets perform going forward, this time, however fiscal policy definitely stands a chance.

Pingback: Money on the sidelines? | BeyondOverton