Tags

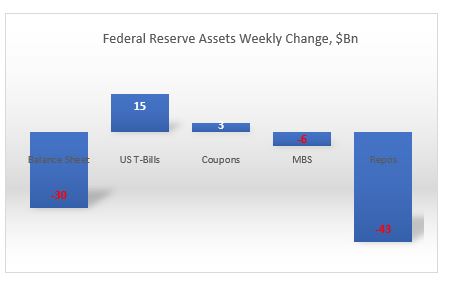

Total assets down $30Bn: the biggest weekly decline since May 1, 2019, and down $27Bn from peak on Jan. 1, 2020. All of the decline is on the back of repos, down $43Bn on the week, and 70Bn from peak. At $186Bn, repos were last time here in mid October 2019.

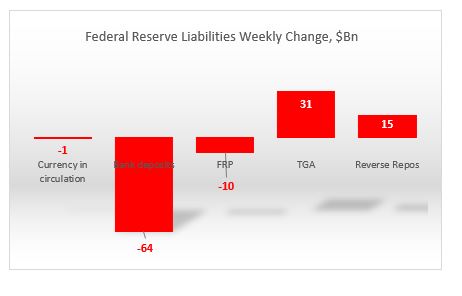

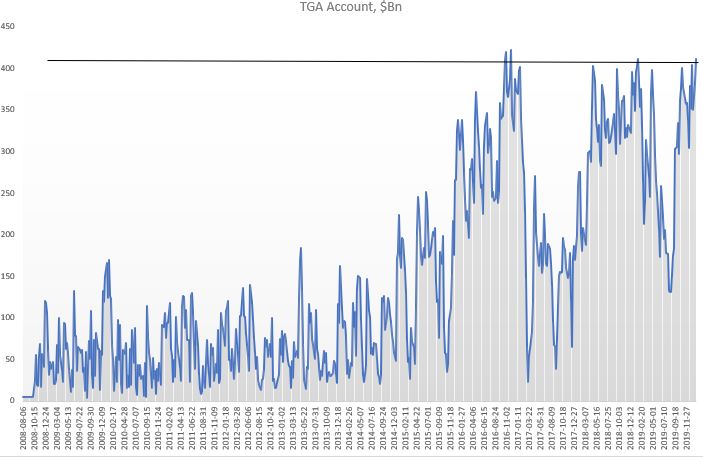

On the liability side, bank reserves declined by $64Bn. But the liquidity dropped more because both the TGA and domestic reverse repos rose by $31Bn and $15Bn respectively. At $412, TGA is at its highest level over the last 12 months. On the other hand, and as expected, FRP continues to decline and at $250Bn is close to the low end of the 12m period. Currency in circulation also dropped for third week in a row, posting the biggest cumulative decline from its peak over the last 12m. The decline in FRP and currency in circulation cushioned the otherwise drop in overall liquidity.

Going forward, there is no doubt that the bulk of the central bank’s increase in balance sheet is behind us for the moment, ceteris paribus. The Fed will continue shifting from repos to T-Bills and probably coupons (especially if it hikes the IOER/repo rate next week). The effect on liquidity will depend on the liabilities mixture, though. Expect TGA to slowly start decreasing ($400Bn has kind of been its upper limit, rarely going above it by much).

FRP has a bit more to go on the downside but I think it will struggle to break $200Bn, probably settle around $215Bn.

That should help liquidity. If the Fed buys more securities than the decline in repos, under that scenario, bank reserves/liquidity go up. If not, it really depends on the net effect of the change in autonomous factors.

If you are trading Fixed Income, expect a bit more pressure on the curve to continue flattening. If you are trading equities, none of this matters to you. At the moment, the only thing the equity market cares about is the size of the gamma cushion.