Initially published on MacroHive on February 6, 2020

In light of the vertical rise in Tesla’s share price in the last few months, I thought it worthwhile to revisit an old narrative comparing the Apple’s iPhone moment with Tesla now. My verdict: I wouldn’t get sucked in by any ‘paradigm shift’ just yet. Though there are plenty of possible reasons and even more conspiracy theories, this share price spike is likely nothing other than mad short covering.

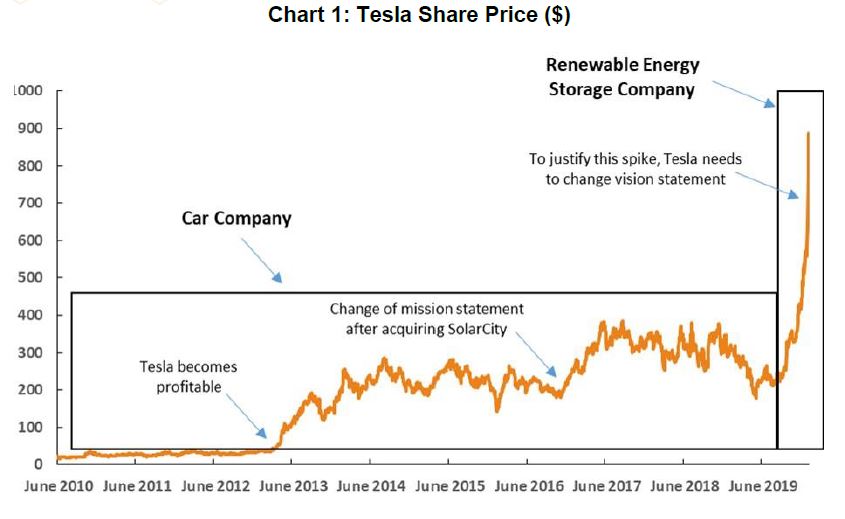

Having said that, Tesla might be worth this much – indeed maybe even more. But the story has to change: Tesla is not a car company, and it is not in the mobility business; instead, it is an energy storage company, and it is in the renewable energy business.

The iPhone shifted the paradigm because it distinguished itself as a mobile device, not a mobile phone. Moreover, the iPhone arrived at the very beginning of the internet/social media/digital cycle. Tesla is still a car (you need to drive it!), albeit without an internal combustion engine, and it comes at the end of the mobility cycle. After all, cars have been around in roughly the same form for at least 100 years. Air travel was a much bigger disruptor. If you want an iPhone analogy in the mobility cycle, it’s that, not Tesla. The fact that air travel is a money loser now also supports the idea that we are at the end of the traditional mobility cycle.

The Autonomous Vehicle (AV) could be the next big disruptor in the mobility sector, not the Electric Vehicle (EV) – which is what Tesla currently is. People are much more likely to use an AV than an EV because in an AV they are free to do whatever they want while it transports them. It also has the potential to be cheaper and more comfortable than a driver-operated EV taxi.

The problem with AV, still, is that it is a long way off. Elon Musk had initially set a deadline of fully autonomous driving by the end of 2019. That obviously did not happen. During the company’s Q4’2019 earnings call, Musk said that it might happen in a few months. But he downplayed how well the system would work, clarifying, “That doesn’t mean the features are working well”. This is not just a question of technology (for example, given the complexity of the urban landscape, city driving requires fully Level 5 automation), but it is also a question of regulations and costs. By the time the fully AV is available, probably not before the 2030s, especially in urban settings, the demand for it, will likely be lower simply because the digital medium would have evolved much more, surpassing the physical medium in terms of popularity.

So, if Tesla is not at its ‘iPhone’ moment, what could justify such a high share price?

As a car company, the $150bn market capitalisation makes little sense given comps in the industry. Though the last three quarters have finally been cash-flow positive, if the latest number of $976mm is properly discounted by the stock-based compensation of $898mm (accounted as a non-cash cost), the free cash flow (FCF) is not that big. And bear in mind that to get to it, Tesla had to halve its initial 2019 CAPEX from $2.5Bn, projected in Q1’2019, to what came to be the real 2019 number of $1.3bn. With one of the lowest CAPEX as a percentage of revenues in the business, it is difficult to imagine how Tesla will compete with the other car producers.

Tesla as a software company (similar to Uber and Lyft, i.e. turning into a utility as a platform) could possibly push the valuation up a bit, but hardly to where we are now given that Uber’s market cap is less than half of Tesla’s. The only way to get to the escape velocity we have been experiencing in the share price now is to completely exit the mobility sector and to focus on energy storage as the missing link in our society’s transition to a renewable energy future.

There is an argument to be made that this could have been Elon Musk’s initial idea. In 2004, less than a year after founding Tesla, Musk and his cousin thought of starting SolarCity during a trip to Burning Man, realising solar power’s potential in countering climate change. Tesla acquired SolarCity in 2016 and, in that same year, the company’s mission statement changed from ‘transitioning the world to sustainable transport’ to ‘accelerate the world’s transition to sustainable energy’.

But still, to get to today’s valuation, Tesla would have to put on a smart PR exercise talking about this mission statement shift in detail. To go higher from here, Tesla would need to align its vision statement, ‘to create the most compelling car company of the 21st century by driving the world’s transition to electric vehicles’ to its mission statement above. i.e.Tesla

needs to completely drop the transportation angle (where margins are only going lower) and invest a lot more in CAPEX and R&D with a focus on developing the best renewable storage options.

If then the market understands where Tesla is committed to going and believes in its technological abilities, it will drop all its requirements for near-term profitability and start pricing the stock with a much higher multiple – one more in line with other near-monopoly companies with a first-mover advantage. Barring any such efforts, Tesla’s stock is probably heading down as soon as the short covering is finished. At the end of the day, valuations are a matter of perceptions and assumptions first, and only then a question of whether the numbers fit. Wednesday [February 4] saw the start of this correction with a 17% drop. The only question now is whether the selloff will be as fast as on the way up.