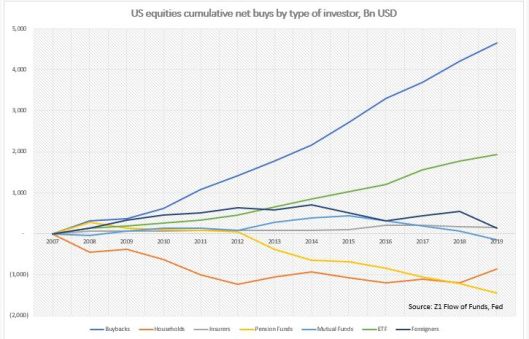

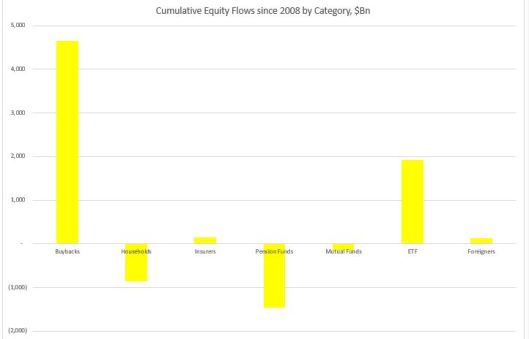

1.Net cumulative real money equity flow (households, mutual funds, pension funds, insurers and ETFs) is down almost $400Bn since 2008.

2.There is a clear trend obvious above of switching from active equity management (households, mutual funds, pension funds, insurers) to passive (ETFs).

3.The only real buyer of equities since 2008 are non financial corporates themselves. Although, to be fair, the domestic financial sector has been a large issuer of equities, especially immediately post 2008, offsetting some of the demand from corporates. Bottom line is that since 2008, very generally speaking, real money has been selling equities into a corporate bid.

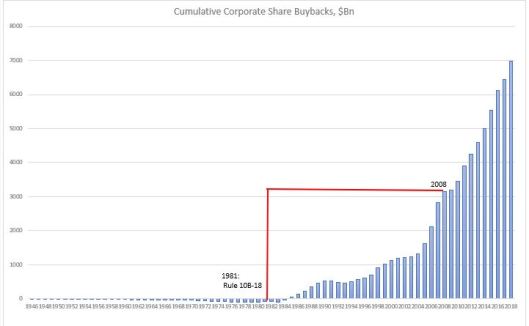

4.Share buybacks started in earnest only after SEC Rule 10B-18 was introduced in 1981. Until then corporates were net issuers of shares (supply increased). After 1983, on a cumulative basis, corporates became net buyers of equities (supply shrank). From 2008 onwards, corporates bought back more shares than for the whole period before.

5.Households have been reducing their direct holdings of equities. From 1946 till the early 1990s they moved from owning direct to owning equities through their pension fund. From 1990 till 2000 they expanded also in mutual funds and as a result, the growth of pension funds’ exposure to equities slowed down at the expense of mutual funds growth. And from 2000 till now they have been switching further into owning equities through ETFs at the expense of all of the above.

6.Since 2008, cumulative equity inflow from insurance companies and mutual funds is more or less flat. Pension funds divested from equities at the expense largely of ETFs.

7.Equities inflow from foreigners really picked up after 2000s but peaked in 2014.