Tags

Things the Fed can do to alleviate the potential repo squeeze (apart from the usual suspects already discussed in great detail by both saleside/buyside research and in Twittersphere):

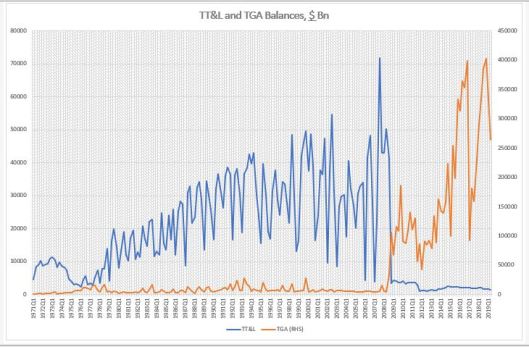

1) hike the interest banks pay on TT&L ‘notes’ accounts from EFF-25bps to EFF, or to make it even simpler, equal to IOER. That could encourage funds to move from the TGA account back to TT&L accounts and ‘release’ reserves.

When the Fed started paying IOER, the opportunity cost for the Treasury to keep money on deposit in the banking system (TT&L accounts) rose. The Treasury thus started using the TGA at the Fed.

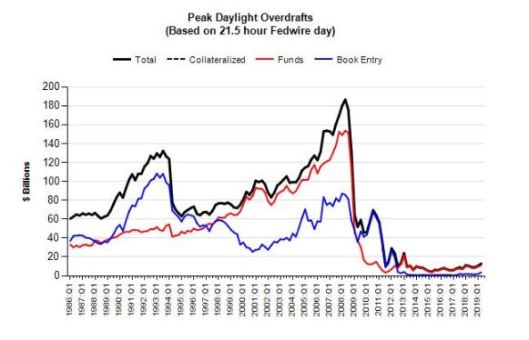

2) cut the fee on daily uncollateralized overdrafts from the current 50bps, adjust the net debt caps, decrease the penalty daily overdraft fee of 150bps. That could encourage better use of the existing Fed intraday liquidity option.

The Fed made major changes to its daily overdraft operations in 2011 spurred by some inexplicable desire to limit its credit exposure. This was probably on the back of political pressure from the legacy of the 2008 crisis during which the Fed indeed took massive credit risk.

Before 2011, the majority of the Fed’s daily overdrafts were uncollateralized. The new rules discouraged uncollateralized ‘repos’ by raising their fees and introducing collateralized overdrafts for free. After those changes, majority of the overdrafts became collateralized. The problem arose when during the most recent repo squeeze, the mechanics of obtaining collateral became complicated.

In any case, Fed’s action was strange given the fact that only a few months before that, in 2011, it had changed the accounting rules which pretty much ensured that the central bank can not go bankrupt (no negative equity) even in theory.

Should the Fed, actually, be providing free intraday liquidity with no collateral to eligible institutions? I think so. Because:

-that liquidity is needed for transaction (retail 24/7), not consumption or production purposes (Pfister 2018)

-the central bank can create money at zero cost, while the opportunity cost of holding money should be equal to the social cost of creating it (Friedman 1969)

-the central bank would be simply accommodating Basell III regulations

These two solutions are not groundbreaking: the Fed would be either going back to the way things were before 2007 (uncollateralized Fed daily overdrafts), or taking into account new developments (the emergence of IOER).