(Click to enlarge)

This is a follow-up on yesterday’s post which showed a simplified version of the hierarchy of money. This one dwells on why exactly the money supply is not reaching the end consumer and how this can be fixed.

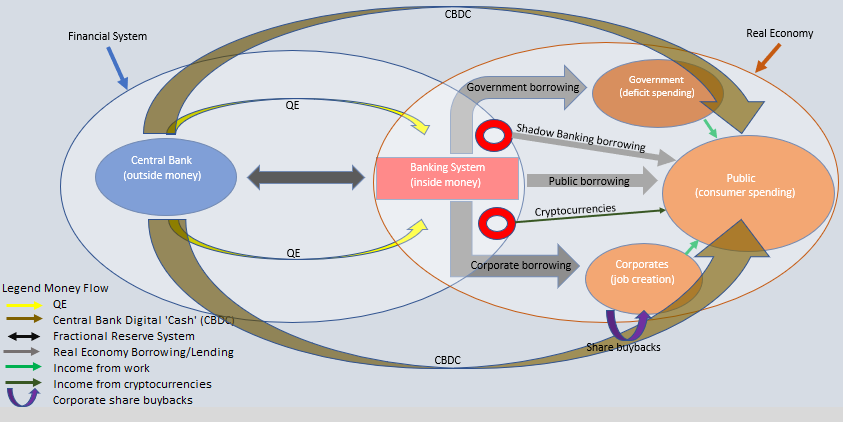

The two main parts of the diagram are the financial system and the real economy. The financial system comprises all the main actors depicted in the “Hierarchy of Money”: the central bank, the banking system, shadow banks and cryptocurrencies. The link between the financial system and the real economy is the banking system (with the help, recently, of shadow banks and cryptocurrencies).

At the moment there is no direct way to ‘deliver’ safe assets from the central bank to the public. Everything has to go through the banking system which generates state-backed private money (the banks and the shadow banks) which then get lent to the public. Cryptocurrencies are a new addition to the financial system. Unlike the other actors, they generate private assets not backed by state money and, moreover, they can enter the real economy directly, not in the form of borrowing but in exchange for ‘work’ (the verification process) – which is what really makes them attractive to the other forms of money.

The process of QE is really a closed-loop within the financial system. All it does is swaps financial assets (mostly sovereign paper in the US and UK, some private assets in EU, and now a lot of private assets in Japan) for central bank reserves. The public does not get any benefit from QE directly. However, they do benefit from the lower rates of interest, thanks to QE, which the banks offer on borrowing (the downside being that demand for loans has decreased in the developed world after 2008 in general, and, moreover, banks are not that eager to extend new loans pressed by the recent regulations).

Within the real economy, there are generally two traditional ways to receive income: from corporates and from the government, in both cases in exchange for work. Working for the government had been on the rise before 2008 but with the push for austerity thereafter, this has slowed down. Corporate employment has remained stable but because of outsourcing abroad and especially because of technological automation of work, real wages have been stagnant for decades. Higher paid manufacturing jobs have been replaced by lower paid service jobs; full employment with benefits has been replaced by part-time employment without benefits.

In addition, corporates had been investing less and less in R&D and Capex, which in theory could have led to more employment. In fact, since 1982 when Rule SEC 10B-18 was introduced, corporate have preferred to engage in share buybacks.

So, one way for the public to replace the lost income from traditional employment has been direct borrowing from the banks. This is a phenomenon which started already in the 1980s with the financialization of the real economy. It really took off after the dotcom crisis when shadow banking offered cheap residential mortgages loans. After 2008, which marked the peak of the private debt super-cycle, this has also slowed down massively.

This opened the way for cryptocurrencies to fill in the void offering an alternative source of income – access to a seemingly safe private asset. Cryptocurrencies are a much riskier development than the shadow banking lending and if they are allowed to spread more widely within the real economy, they could lead to a much bigger financial crisis than 2008.

The economy cannot operate if all avenues which increase consumer purchasing power are either closed (Work≠Job≠Income) or they are becoming risky (direct borrowing from banks, shadow bank borrowing, cryptocurrencies). The public needs to be able to receive safe assets directly from the central bank (central bank digital ‘cash’) either in the form of discounted loans or even in the form of UBI.

Pingback: ‘State’ money creation – this ghost from the past is badly needed for the future | BeyondOverton

Pingback: The type of credit creation matters | BeyondOverton