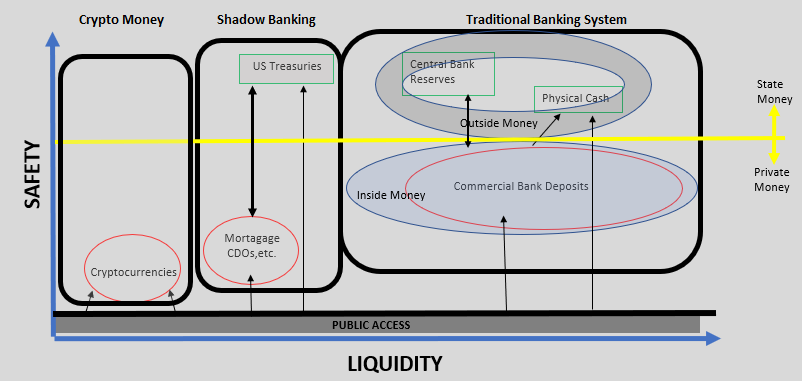

This is a simplified diagram of the modern monetary system from the point of view of liquidity (horizontal axis – liquidity increases as we move to the right) and safety (vertical axis – safety increases as we move upwards). It distinguishes among three types of monetary systems: traditional banking, shadow banking and crypto money. In addition, it defines money as ‘private’, i.e. money created in the private financial system (majority of money) and public or state, i.e. money created by the central bank or the government. Finally, the diagram shows which type of money the general public has access to at the moment.

This is work in progress, any feedback is welcome!

Traditional Banking System

The traditional banking system is centralized with the central bank sitting at the top issuing central bank reserves. To connect to the major payment systems, such as BACS or CHAPs in the UK or Fedwire in the US, financial intermediaries must have a reserve account at the central bank. Generally speaking, because central bank reserves are used only for settlement purposes between the central bank and commercial banks, they are sometimes called ‘outside’ money, i.e. money which sits outside of the real economy: the general public does not have access to them.

‘Outside’ money has gone to also comprise all state-issued money: in the US this is the physical coins issued by the government (the US Mint) and the paper dollars issued by the Federal Reserve (US Bureau of Engraving and Printing). It is only to this state money that the general public has access to. ‘Outside’ money is the safest money instrument out there: a fully sovereign government can never willingly default. The risk, as always, is only inflation.

Below state money lie commercial bank deposits which is private money created out of thin air on the back of public borrowing. This privately issued money comprises the majority of money in the system. Because of that, it is also called ‘inside’ money, i.e. this is the money that circulates within the real economy.

Commercial bank deposits are not as safe as state money because banks can go under (the money created is on the back of loans which are inherently risky). However, through the fractional reserve system which we have in place, part of that money is ‘backed’ by state money, i.e. every single time the commercial bank issues a loan by creating bank deposits it has to make sure it also has (or acquires/borrows) a portion of central bank reserves at the same time. In addition, some portion of the public deposits is insured by the state, so that even if a commercial bank goes bankrupt, some of the deposits will be made whole. Finally, all commercial banks are regulated by the central bank and subject to capital, liquidity and leverage requirements.

The public generally does not dwell much on the riskiness of commercial bank deposits. Except for Northern Rock in the UK in 2008, we have not had many major bank-runs in the developed world since the Great Depression. In fact, to most people who have deposits well below the insurance limit, commercial bank deposits are safe. It is this inherent link to the state which gives this impression of safe commercial bank deposits. In the words of former Bank of England governor, Mervyn King, “[M]any treat loans to banks as if they were riskless. In isolation, this would be akin to a belief in alchemy – risk-free deposits can never be supported by long-term risky investments in isolation. To work, financial alchemy requires the implicit support of the tax payer.”

The money created within this traditional banking system is the safest and most liquid form of modern money.

Shadow Banking

Shadow banking has been around for a while. In fact, in the mid-1990s, shadow banking liquidity in the US surpassed traditional banking liquidity. This, plus the fact that it is not part of the traditional monetary transmission mechanism (a lot of the liquidity created until 2008 was off banks’ balance sheets – not easy for regulators, or for that matter even bank analysts to spot it), contributed to the 2008 financial crisis. Since 2008, however, shadow banking liquidity has massively declined and now is again less than traditional banking liquidity.

In a similar fashion to the traditional banking system, the core of the shadow banking system is a state money-like asset: US Treasuries. The actual ‘money’ in the shadow system is also, similarly, a private asset in the form of a repackaged loan: the mortgage CDO/CBOs. US Treasuries are used as collateral for the mortgage packages, or one could say as settlement instruments not unlike the central bank reserves. Unlike in the traditional banking system though, the public has direct access to the US Treasury market.

The safety of the US Treasuries is on par with the safety of the state money in the traditional banking system. In terms of liquidity, it depends on the usage. The mortgage packages, however, are private ‘money’ which are substantially less safe than the private commercial bank deposits of the traditional banking system (even though, in most cases, the former had actually higher ratings, a fact which was at the core of the mortgage crisis of 2008).

The shadow banking system grew out of the inadequacy of the traditional banking system to distribute money efficiently. It was a perfect timing as well, coming on the heels of the dotcom crash when the authorities were more than eager to see the residential real estate market driving the bounce.

Crypto Money

This is the latest development in the transformation of the modern monetary transmission mechanism. In a similar fashion to the rise of the shadow banking system in the early 2000s, crypto currencies have come in to fill in the void of lost income post the 2008 crisis and the inability of modern money supply to reach the end consumer.

Crypto money is even worse (less safe) than shadow money because it lacks state money collateral. In addition, the private asset is created outside of the private financial system in a decentralized/distributed fashion. However, its claims of ‘equality’ when it comes to money creation (a permission-less system) may have been valid in the beginning, but with the complexity of the verification process increasing and the need for extra computer power, it is not the case any longer: a few ‘miners’ are now ‘in control. The hard forks which have happened in Bitcoin are an example of these vested interests.

Finally, on the positive side as this is the whole point, the public does have access to cryptocurrencies, but with their price having risen several times over just this year, reality is that now only the ‘privileged’ can afford to buy the major cryptocurrencies. And because they are considered a store of value, with a lot of buyers claiming they are going to hold them ‘forever’, cryptocurrencies are much less likely to be exchanged and thus their liquidity will continue to suffer.

Access to central bank balance sheet

The sovereign state through the central bank is the only issuer of safe assets. Ironically, in the process of QE with the aim to prop up the deleveraging banking system, the amount of safe assets has been greatly reduced (the central bank buys sovereign bonds, to which the public has access to, and issues reserve balances to which the public does not have access to). The demand for physical cash has actually risen in the developed world, partially on the back of this.

In fact, the central bank or the government does not have direct control over any of the safe assets the public has access to: coins are issued by the government and paper dollar are issued by the Federal Reserve but only on the back of demand for physical cash by the public (the public swaps electronic commercial bank deposits with physical cash – in other words, there is no mechanism by which the central bank/government can give physical cash to the public unless it passes through commercial bank deposits). US Treasuries are issued by the government but again they can generally be purchased only by swapping them with commercial bank deposits.

Because access to its balance sheet is so restricted, the central bank’s efforts to increase monetary liquidity post the 2008 financial crisis have been highly inadequate. In fact, in light of this, the central bank should have focused more on how to directly help the financial system with its deleveraging process, than on affecting the money supply. To that effect, it would have been much more beneficial for the central bank to focus on buying mostly private assets. Both the BOJ and ECB have eventually started doing this but more on the back of declining supply of sovereign paper rather than by design.

In addition, the ability of commercial banks to increase the money supply is severely limited not only because there is less borrowing demand from the public but also because capital and leverage regulations (Basel III) make it prohibitively to do so. So, as the money transmission mechanism stalls, similar to the period post the dotcom crisis in the early 2000s, the market has gone and created alternative private safe assets to supplement the public’s need for money: this time, cryptocurrencies. Because they are even more toxic than the sub-prime mortgage packages, the more widespread they become with the pubic, the higher the risk of an even bigger-than-2008 financial accident.

The answer could be widening out access to the central bank balance sheet for the whole population. This can be done in various ways using the same blockchain technology now prevalent amongst the various cryptocurrencies. Indeed, a previous post listed some of the major central banks and their efforts in this direction.

Pingback: A simplified version of the monetary transmission mechanism | BeyondOverton

Pingback: ‘State’ money creation – this ghost from the past is badly needed for the future | BeyondOverton

Pingback: A look at shadow banking globally | BeyondOverton