Credit impacts the real economy in a different way depending on whether it is to households or to corporates (see Atif Mian’s work, also his interview here). Very generally speaking, credit to households affects the economy directly through the demand-side channel, while credit to corporates – through the supply-side channel directly, and only then, potentially, indirectly through the demand-side channel.

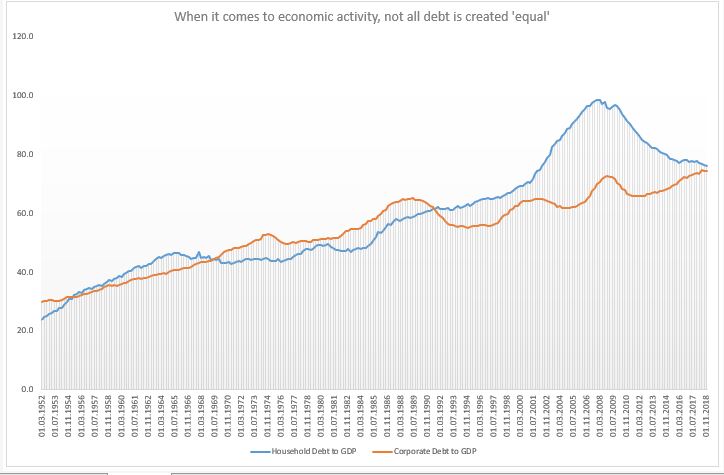

Household debt to GDP was flat for two decades between mid-1960s and mid-1980s; and then it doubled; corporate debt for GDP, on the hand, was flat also for two decades after the S&L crisis, and even now it is only a few per cents higher. But the demand-side reduction from the household debt channel post 2008 is rather unique.

Given that the US was running a negative output gap for most of the period post 2008 (and it might still do, even though official estimate is for a small positive), it was the demand-side that needed some catching up to. Instead, the opposite was essentially happening: credit to households was decreasing relative to credit to corporates. As far as credit was concerned, it was primarily the supply side that was getting stimulated (of course, the question is how much stimulus was really created given that a lot of the corporate debt went to share buybacks).

The other theory, one to which I subscribe, is that the modern economy is essentially always experiencing a demand gap. When real wages stopped growing in the 1990s, post the the financial liberalization of the 1980s, household credit experienced a massive run-up. The demand gap left from the stagnation in real incomes was filled with household debt. Until the sudden stop in 2008.

Household debt to GDP did not grow between 1960s-1980s but real household income did, so there was no demand gap either. Post 2008, though, neither of these two options were available which left the US economy in a demand insufficiency. The ‘stimulus’ provided was mostly through the supply side with very little follow through into the demand side which meant lackluster economic growth.

The bottom line is that the type of credit creation matters. The central bank affects directly only the supply of credit (and in some cases, even less so) thus, it has limited ability (none?) to decide on whether credit goes to firms or households. We may get a lot more from lower interest rates if policy makers start thinking more holistically about the whole process of credit creation. Banks do not care where credit goes (why should they?) as long as they get their money back.

But with overall debt in the economy climbing higher and higher, it is essential to think how we can get the most out of it. And if the market can’t do that (it can’t), someone else should step in.

All this does not mean that US households should get even more indebted! On the contrary, the decline in household debt to GDP is good news only if it were also followed by a similar rise in real household income. And it the private market can’t do that either (it seems, it can’t), then we need to rely on the official sector to take on that burden.