- Either the peak in the Fed Funds rate is much higher, or the UST yield curve, 2×10, is too inverted. Whatever the case is, it’s extremely unlikely that the Fed eventually ends up cutting just the 150bps priced in at the moment.

- Or to be more precise, unless there is a modern debt jubilee (a central bank/Treasury debt moratorium) or a drastic capital destruction caused by a total collapse in the global supply chains, continuation of war in Europe/Asia or a natural disaster (climate change, etc.), the Fed is more likely to pause the hikes next year, wait, and eventually cut by more than the 150bps priced in the market but less than in the past.

- In other words, the shape of the current Eurodollar curve is totally ‘wrong’, just like it had been wrong in the previous three interest rate cycles but for different reasons.

The current UST 2×10 curve inversion is pretty extreme for the absolute level of the Fed Funds rate. At -70bps, it is the largest inversion since October 1981 but back then the Fed Funds rate was around 15%. The maximum inversion of the UST 2×10 curve was -200bps in March 1980 when the Fed Funds rate was around 17%. The Fed Funds rate reached an absolute high of almost 20% in early 1981.

Back then the Fed was targeting the money supply, not interest rates, so you can see the curve was all over the place and thus comparisons are not exactly applicable. But still there were plenty of instances thereafter when the Fed moved to targeting the Fed Funds, and the Fed Funds rate was much higher than now, but the curve was much less inverted before the cycle turned.

Take 1989 when the 2×10 UST curve was around -45bps but the Fed Funds rate at the peak was around 10% (almost double the projected peak for the current cycle). The Fed ended up cutting rates to almost 3% in the following 3 years. Or take the peak in Fed Funds rate in 2000 at 6.5% and a UST 2×10 yield curve inversion of also around 45bps. The Fed proceeded to cut rates to 1% in the following 4 years.

Finally, take the peak in Fed Funds rate at 5.25% in 2006-7 and a UST 2×10 yield curve inversion of around -15bps. The Fed ended cutting rates to pretty much 0% in the following 2 years. In the 2016-18 rate hiking cycle, when the Fed Funds rate peaked at 2.5%, the UST 2×10 yield curve never inverted.

So, today we have a peak in the Fed Funds rate of around 5%, so comparable to the 2007 and 2000 cycles, but a much deeper curve inversion, more comparable to the 1980s. If we go by the 2000 and 2007 scenarios, the Fed cut rates by around 500bps; in the 1980s the Fed cut much more, obviously, from a higher base. In this cycle, if the peak is indeed around 5%, 500bps is the maximum anyway the Fed can cut. That is also the minimum which is “priced in” by the current curve inversion. But the actual market currently and literally prices only 150bps of cuts.

Again, neither of the past interest rate cycles are exactly the same as the current, so straight comparisons are misleading, but somehow, it seems that the peak Fed Funds rate today plus the current pricing of cuts in the forward curve do not quite match the current UST 2×10 curve inversion – either the peak is too low, or the curve is too inverted.

What I think is more likely to happen is the Fed hikes to more or less the peak which is priced in currently around 5% but it does not end up cutting rates immediately. The market is currently pricing peak in May-June next year and cuts to start pretty much immediately after; by the end of 2023 there are 50bps of cuts priced in.

In the last three rate cycles (2000, 2008, 2019) there was quite a bit of time after rates peaked and before the Fed started cutting. The longest was in 2007 – 13 months, then in 2019 it was 8 months and in 2000 it was 6 months. Before 2000 the Fed started cutting rates pretty much immediately after the end of each rate hiking cycle, so very different dynamics.

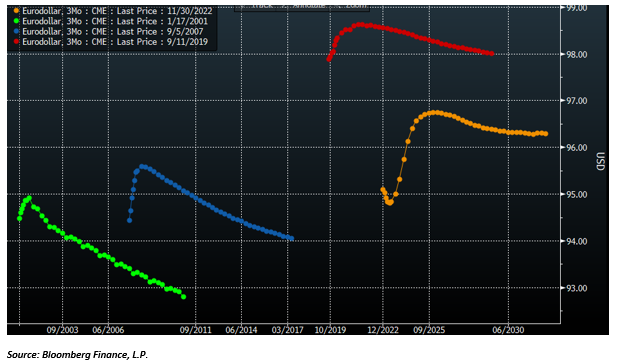

Here are how the Eurodollar curves looked about six months before the peak in rates in each of these cycles. The curve today somewhat resembles the curve in 2006, in a sense that the market correctly priced the peak in rates in 2007 followed by a cut and then a resumption of hikes. But unlike today, the market priced pretty much only one cut and then a resumption of hikes thereafter. In the interest rate cycles in either 2000 or 2018 the market continued to price hikes, no cuts at all, and a peak in the Fed Funds rate not determined.

Source: Bloomberg Finance, L.P.

And here are how the curves looked after the first cut in each of these cycles (the colours do not correspond – please refer to the legend in the top left corner, but the sequence is the same – sorry about that). The market didn’t expect at all the size of cuts that happened in either of these cycles. Notice that the curve in the current cycle still does not look at all like any of the curves in the previous cycles (noted that in six months’ time, the current Eurodollar curve is also likely to look different from now, but nevertheless, there are much more cuts priced now than in any of the other three cycles).

Source: Bloomberg Finance, L.P.

The point is that the market has been pretty lousy in the past in predicting the trajectory of the Fed Funds rate.

- It is strange that the market never priced the pause in any of the actual past three interest rate cycles, and it is even stranger that it is not pricing it now either, given that there has been consistently a pause in the past.

- In none of the past three cycles did the market price any substantial cuts; in fact, we had to wait for the first actual cut for any subsequent cuts to be priced – that is also weird given that the Fed ended up cutting a lot.

- This time around, the market is pricing more cuts and well in advance but not even as close to that many as in the previous cycles.

However, I do not think we go back to the zero low bound as in the past three cycles. To summarize, the current UST 2×10 yield curve is too much inverted and the Fed would eventually cut rates more than what is currently priced in, but much less than in other interest rate cycles and after taking a more prolonged pause.