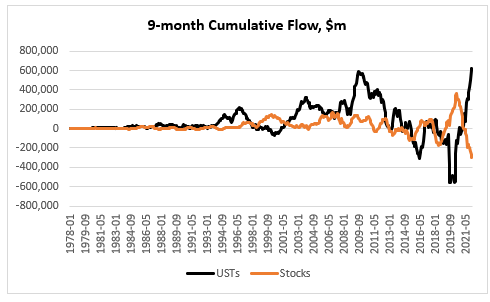

Foreigners have bought record amount of USTs this year: if we look at the nine-month cumulative flow in USTs (YTD as per TIC data), it is at a record high, marginally beating 2009. This is actually in stark contrast to what they have done with US equities: the nine-month cumulative flow in stocks is at a record low, easily beating the previous low in 2018.

While it is more difficult to compare stocks across countries, as there are a lot more idiosyncratic factors at play, with bonds it is a little bit more straightforward, once we take hedging costs into consideration. And by that measure, USTs are the most expensive they have been at least in the last 10 years.

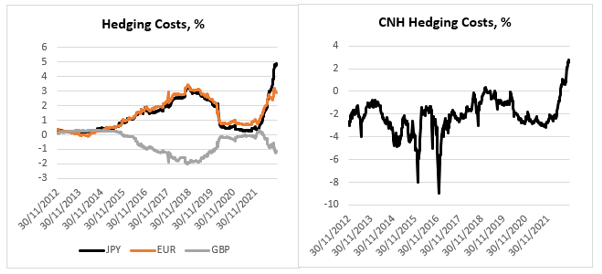

Here at the USD hedging costs for foreign based investors based in these jurisdictions (the calculation is done using 3m FX forward points and – so, an investor buys USD and immediately sells it 3m forward – converted into a ‘yield’/carry, annualized). I have chosen here the largest foreign buyers of USTs: Japan, China, the United Kingdom, and Europe (I have excluded the Cayman Islands which is another large buyer of US assets because even though classified as a foreigner in the TIC data, the hedge funds there are almost all USD-based).

Hedging costs in Japan and China are the highest in the last 10 years; hedging costs for EUR-based investors are close to the highs; hedging costs for GBP-based investors are substantially off their highs. This is what a foreign investor is getting in yield if he or she invests in UST 10yr.

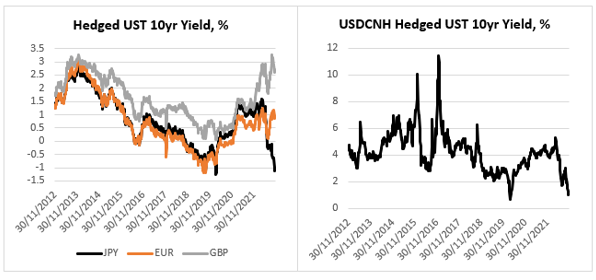

This is in nominal terms – do not be confused by the fact that a JPY-based investor will receive a negative 1.2% yield if he or she invests in UST10yr hedged into JPY for one year. A European would do slightly better, and a Brit would do even better than a European; in fact, until recently a Brit buying USTs hedged in GBP could have picked the highest yield in the last 10 years!

But USTs are really not that attractive anymore to a CNH-based investor – even though he or she still picks up a decent 1% hedged, which is more than a European would gain, this is the second lowest yield in the last 10 years. In fact, this is the same for a Japanese investor – the only other time UST10yr fully hedged yield has been lower was during the height of the Covid crisis in 2020.

Foreigners are much better off buying their own government bonds than UST10yr, if they do indeed hedge the currency risk. In almost all these four cases (GBP is the exception but only recently) foreign bonds offer a record pick up to fully hedged USTs.

So, how do we reconcile the record buying of USTs YTD by foreigners with these findings? First, the hedge funds in the Cayman Islands have been large buyers of USTs but, as mentioned above, they are USD-based. Once we exclude them (and they have bought 40% of the USTs from ‘abroad’ YTD), foreign buying of USTs is not that high. UK-based accounts have actually been the largest buyers of USTs from abroad (pretty much bought the other 60% of the USTs). I think some of those accounts in the UK are actually USD-based. There is also the peculiarity of the UK Gilts market this year – about 40% of the total YTD buying of USTs by UK-based accounts happened in the two months before the LDI crisis.

As to the two behemoths in the UST market, Japan, and China, yes, they have been net sellers of USTs this year, in line with what the relative valuation above would have predicted. Where does that leave USTs? Looking at the sectoral balances in the US, the private sector still has a sizable $1.4Tn of surplus (as of Q2 this year), and as we have seen above, USD-based investors have not been shy to pick up these relatively high yields in the UST market.