Tags

April TIC data released.

- Heavy foreign UST selling continues.

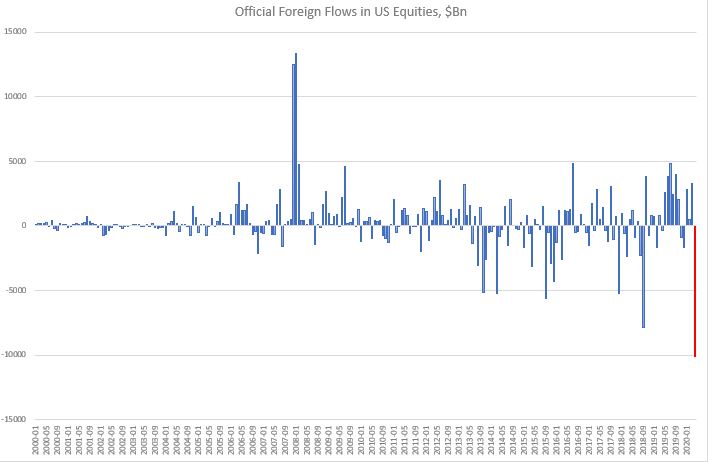

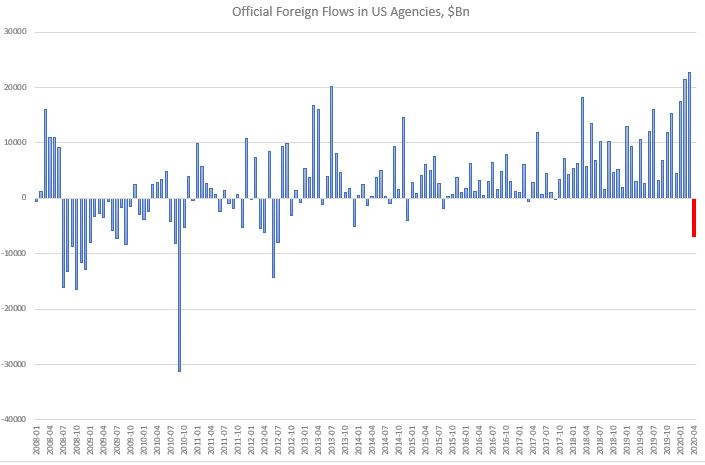

- Foreign selling starts to pick up also in US equities and agencies.

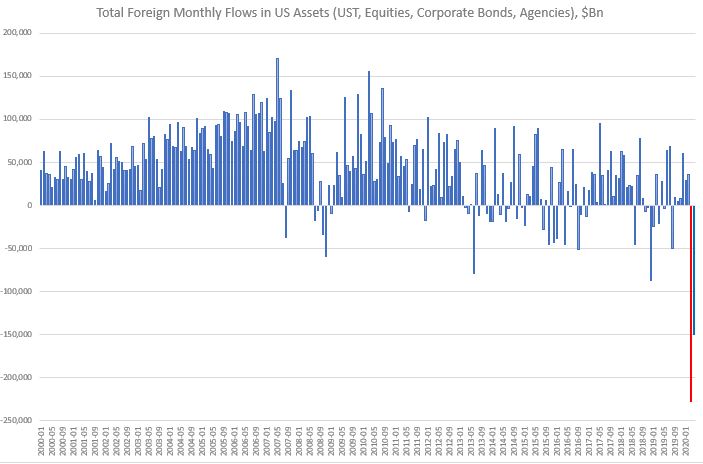

March broke the record for Total foreign monthly outflow.

This happened largely on the back of a record Private foreign sector outflow.

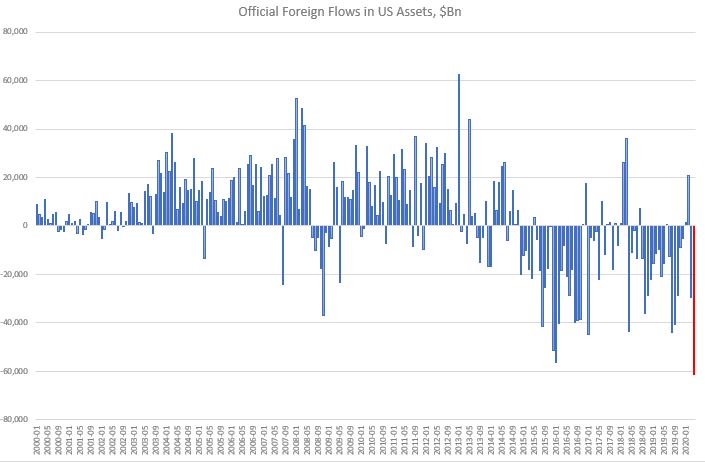

April still saw a large net foreign outflow, though not as big as March. Nevertheless, this time, the Official foreign flow reached an all-time low.

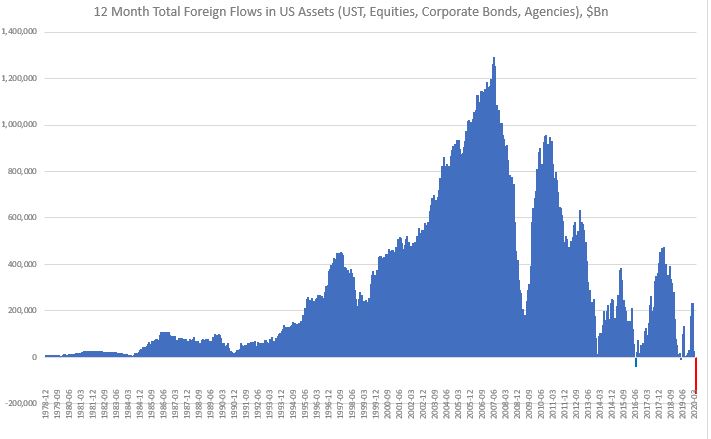

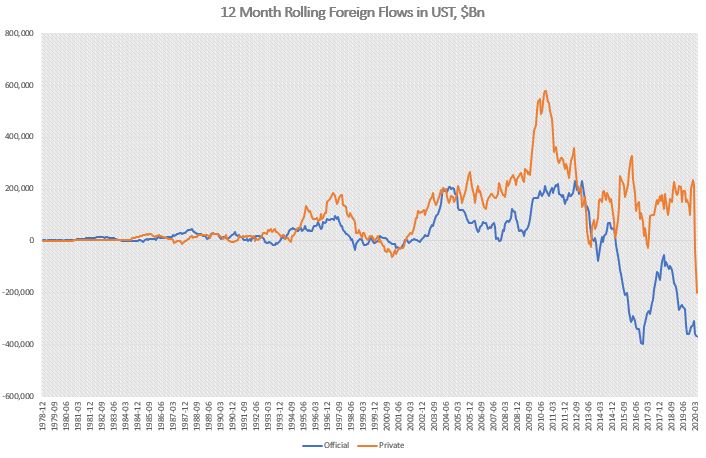

This is significant because the 12-month rolling cumulative total foreign flow in US turned negative by a large amount. This is very, very unusual.

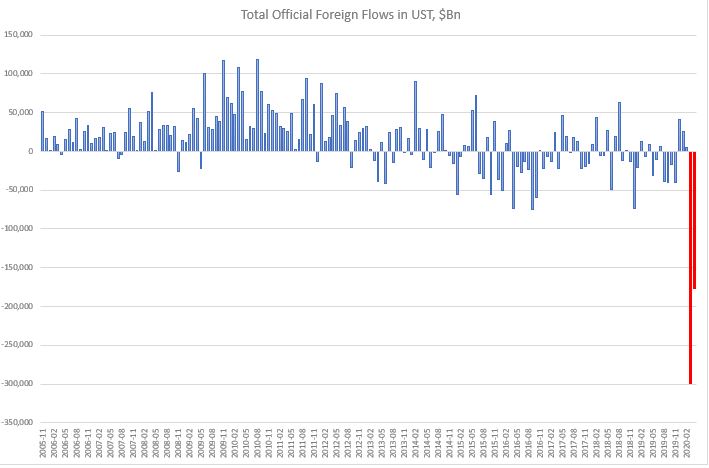

Foreigners are still focused at the moment on selling primarily USTs.

While in the past, private foreign accounts may have bought USTs even when official foreign accounts were selling, in the last two months (April-March), private foreign money turned sellers in size. In fact, their outflows have been several times bigger than the official foreign account outflows. This most recent selling put the 12-month rolling UST private foreign flow in negative territory in March. It reached an all-time low in April. The 12-month rolling UST official foreign money flow is also close to its all-time record low, reached in November 2016.

On the US equities side, unlike in March, though, this time foreigners were net sellers. The total outflow was not that large by historical standards, but the official foreign outflow was.

Foreigners continued to buy US corporate bonds, especially official foreign money. Nothing new there.

Finally, on the agencies side, official foreign accounts were a rather unusual and large seller.

Conclusion: The continuous high level of total foreign US assets outflows in April is interesting and could herald a change in trend of previous USD inflows. We can see that by looking at the rolling 12-month data which turned negative in March and is accelerating lower. In theory, there shouldn’t have been any forced pressure on foreign accounts to exit US assets in April, as Fed/Other Central Banks swap and repo lines were already in place. If this continues, the USD may be in bigger trouble than initially thought. See here, here and here.