Tags

Home Depot cuts its 2019 forecast after sales miss; shares drop the most since 2008.

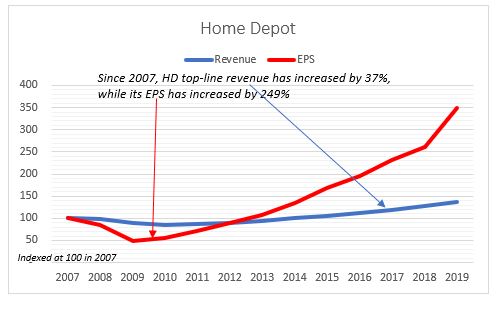

Since 2007, Home Depot’s top-line revenue has increased by 37%, while its EPS has increased by 249%, almost 7x more.

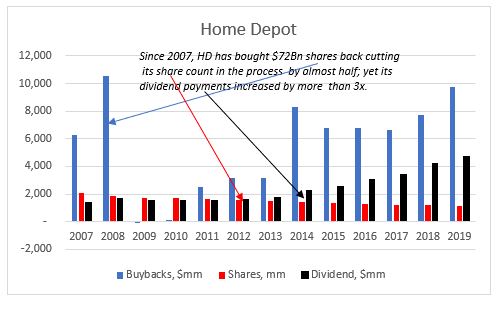

Since 2007, Home Depot has bought $72Bn shares back, one of the largest share buyback programs out there, cutting its share count in the process by almost half; yet its dividend payments increased by more than 3x.

Emphasis on the fact that Home Depot topped analysts’ expectations for earnings but sales fell short. Which is exactly the story of our times: Easier to push up EPS through the share count (buybacks) than through top-line revenue growth. Management also gets paid on EPS, not revenue.

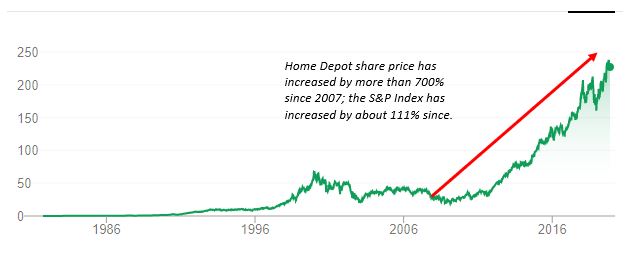

And the cherry on the cake: Home Depot’s share price has increased by more than 700% since the end of 2007; the S&P Index has increased by about 111% since then.

One would have thought that after so many years of Home Depot using the same technique to ‘score a home run’, investors would have understood the tactic and re-priced its valuation.