The bear market in bonds will not arise because of a pick-up in aggregate demand (AD) but because of a possible decline in aggregate supply (AS).

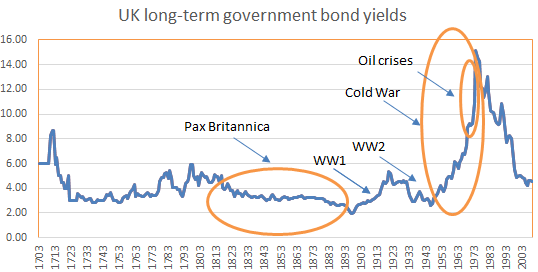

Source: BoE Three Centuries of Data

In times of peace (Pax Britannica see chart above), which allow for capital to accumulate, interest rates trend lower. Wars, conflicts, or even big natural disaster, deplete the capital stock and force interest rates to rise. Sometimes, when these negative supply shocks are one-off occurrences (the 1970s oil crises), we could get just a spike in interest rates; sometimes, if the conflict persists, the increase in interest rates can last much longer (the Cold War).

We are in a period when global capital surpluses have been accumulating at an increasing pace at least since the early 2000s when China entered WTO and most capital barriers were gone. Interest rates have been trending lower since the mid-1980s after the effects of the negative supply shock caused by the oil crises subsided and when eventually, shortly after, the Cold War ended. Some call this the biggest and longest bond bull market in history. It is, probably the biggest because interest rates have gone down from double digits in the 1980s to almost 0% now. But it is certainly not the longest. Interest rates in Britain trended down from 6% to 2% for almost 100 years in the 19th century.

We know that nothing lasts forever in life. Investment trends also end at some point. We spend a disproportionate amount of time and actual and mental capital on predicting these turning points. However, we should probably, instead, heed the words of famous British football coach, Kevin Keagan who is supposed to have said, “I know what is around the corner – I just don’t know where the corner is”. He almost sounds like a portfolio manager when he adds, “But the onus is on us to perform and we must control the bandwagon”.

If we are looking, nevertheless, for the turn in this global bond bull market, we are not going to find it in lower unemployment or even higher wages. In fact, it is unlikely to show up in any economic variables which determine AD. Instead, we should look for signs of any pressure on AS. In an environment of slowing population growth in the developed world and rapid technological expansion, AS can generally accommodate any expansion of AD. However, we should start to get worried if the sustained rise in inequality endangers our institutional infrastructure which leads to a social conflict.

Progress is deflationary. The moment humanity moved from hunter-gathering to agriculture we started creating capital and labor surpluses. Thanks to them we progressed as we could devote extra resources and time to other activities other than survival. At present, when work is equated with a job and income, few people connect that it was because of our leisurely activities that we had a chance to develop the arts and sciences of the past, which defined our culture and laid the foundation of our evolution through history.

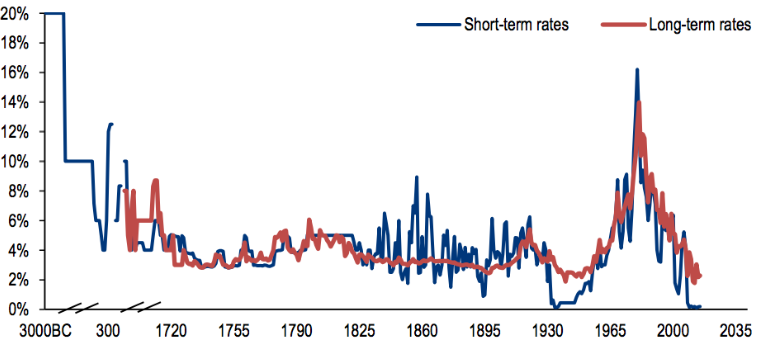

Source: Business Insider; original data from ‘History of Interest Rates’ by Homer and Sylla

Interest rates measure the cost of capital. So, naturally, when capital is abundant, ceteris paribus, interest rates should be low. And even though interest rates have generally moved from the upper left corner of the graph, in Babylonian times, to the lower right corner, now (chart above), history is full of examples when they also go up, and in some cases in a sustained fashion. There could be many reasons for that, but suffice it to say, that any event, natural (earthquakes, floods, etc.) or artificial (wars, epidemic diseases, etc.) which depletes either of the two surpluses would push interest rates higher.

Unfortunately, there have been many more artificial than natural disasters which have delayed our human progress. Nature is unpredictable, but human nature, not so much so. Therefore, some patterns keep repeating in history. Sometimes, it takes years for them to play out but eventually they do. For example, as mentioned above, ever since the Agriculture Revolution, and thanks to the prevalence of capital surpluses, the general norm has been one of AS > AD. The way we have dealt with this s to create an institutional infrastructure to help us distribute the capital surpluses in the most optimal way. Feudalism, capitalism, socialism are some examples of what we have gone through history depending on the level of our economic/technological development.

The problem arises, when a paradigm shift comes around and changes the mode of both production as well as consumption. The Agriculture and Industrial Revolutions are examples of such positive supply shocks which changed the course of our evolution profoundly. In times like these, because of the inertia of the past and numerous vested interests, the institutional infrastructure takes much longer to adjust to these developments. Therefore, as the capital surpluses keep adding up but their distribution mode remains the same, and thus, outdated, the economy becomes more and more imbalanced (AS>>>AD). The point eventually comes when we ‘force’ a change also in the institutional framework to one more suited to deal with these new surpluses.

In the past these changes in societal structure have generally happened through wars and revolutions, a side effect of which has also been a sometimes substantial reduction of the capital (and labor) surpluses. For example, the period between the end of WW2 and now is considered one of general world peace. And indeed, relative to the horrors of the war which preceded it, it was. But despite the fact that indeed there were no major traditional global wars after 1945, the Cold War was a major global war of ideologies, in which few shots were fired, but one which caused a large capital outlay (military build-up, but also huge government investments in space exploration, and in general, technology). In addition, there were a lot of proxy wars (Afghanistan, Korea, Vietnam) and conflicts (for example, the 1970s oil crises were a result of such a proxy conflict). As a result of that, interest rates tended to stay high.

By the end of the Cold War, when it was clear that capitalism had gained the upper hand as the main institutional framework of the time, interest rates started to subside. After the 1980s it was clear that USA was to become the global dominant power. In addition, all these government investments started to pay off and eventually ushered the Digital Revolution which is ongoing right now. To a certain extent, one could think of this period since then as Pax Americana, in reference to the global dominance of Britain during most of the 19th century.

Despite the war on terror, which has required also substantial amounts of capital, the fact that most of the modern world has been in peace, has allowed the proliferation of globalization with trade and commerce booming. Not only the majority of the global surplus capital has found its way back to the US as the default safe haven given its dominance status (and given that the Washington Consensus had made sure most global capital barriers were off), but also it has been US corporates which have hugely benefited from the process of globalization. And finally, US households surplus savings have increased massively. In addition, the Digital revolution could also be ushering a similar paradigm shift to what happened after the Agriculture and Industrial Revolutions in the past.

Source: IMF

Around 60% of these FX reserves are in invested in USD. But is this excess foreign capital trend up now reversing?

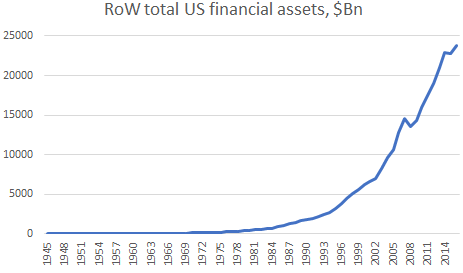

Source: US Federal Reserve Z1 Flow of Funds

The rest of the world (RoW) total US financial assets (market value) have continued to increase. There was an ‘exponential’ pick-up in the late 1970-early 1980s. As of the end of 2016 there was almost $24Tn of foreign money (private as well as public) invested in US financial assets.

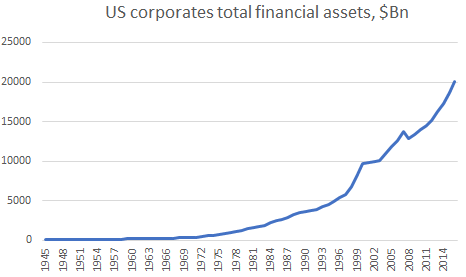

Source: US Federal Reserve Z1 Flow of Funds

As of the end of 2016, US corporates held about $20Tn of US financial assets (of which about $2tn cash).

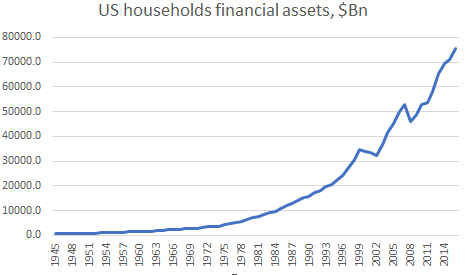

Source: US Federal Reserve Z1 Flow of Funds

Finally, US households hold about $75tn of US financial assets.

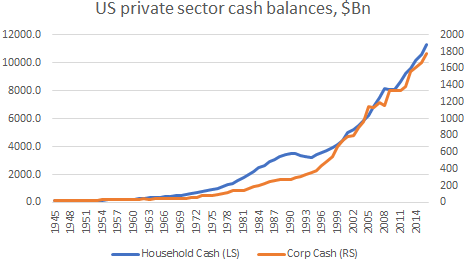

The above numbers are in market value, and market value tends to rise in the long-run as GDP also tends to rise. But even if we strip out the rest and look at nominal cash balances, the US private domestic sector is in huge surplus (chat below).

Source: US Federal Reserve Z1 Flow of Funds

So, it is almost counter-intuitive from what we learn in economics where we are accustomed to believing that a rising GDP is associated with higher interest rates because of the need to suppress potentially inflationary pressures. Reality is that a rising GDP also produces more excess capital which tends to naturally put pressure on interest rates lower. In fact, I wonder whether, if the central banks do not artificially put up base interest rates to supposedly slow down the economy, in an environment of a declining population (slowing AD) growth and an accelerating growth of technological improvements (a large positive supply shock), interest rates would naturally drift lower as GDP rises.