Tags

“For example, it is habitually assumed that whenever there is a greater amount of money in the country, or in existence, a rise of prices must necessarily follow. But this is by no means an inevitable consequence. In no commodity is it the quantity in existence, but the quantity offered for sale, that determines the value. Whatever may be the quantity of money in the country, only that part of it will affect prices, which goes into the market commodities, and is there actually exchanged against goods. Whatever increases the amount of this portion of the money in the country, tends to raise prices. But money hoarded does not act on prices. Money kept in reserve by individuals to meet contingencies which do not occur, does not act on prices. The money in the coffers of the Bank, or retained as a reserve by private bankers, does not act on prices until drawn out, nor even then unless drawn out to be expended in commodities.”

John Stuart Mill, Book III, Chapter VIII, Par.17, p.20

In his latest Global Strategy Weekly, Albert Edwards explains why he thinks the surge in the money supply is deflationary. As usual he is going against the consensus here even though he gives credit to people like Russell Napier who correctly identifies the changing nature of US money supply but concludes that this is highly inflationary. I think Albert is right for the wrong reasons, and Russell is wrong for the right reasons.

Albert Edwards is right when he says that ‘despite massive stimulus, deflation will nimble on for a while yet until capacity constraints become binding further down the road’ (emphasis mine). Yet in his view, deflation will persist because of keeping zombie companies alive by cheap credit. While, I have no doubt that this is invariably true, its effect on the deflation-inflation dynamics is weak because credit creation is now a much smaller part of the money supply than in the past.

Which is where Russell Napier comes in. He is right in his view that ‘politicians have gained control of money supply’ but wrong to believe that this will inevitably cause a rapid rise in inflation unless, indeed, capacity does become binding.

Reality is that money supply is now turned around on its head. While in the past, pre-2008, the delta of money supply consisted mostly of loans, after 2008 and during QE 1,2,3, it moved to loans plus QE-generated deposits. During the Covid crisis, it shifted further away from loans by adding even Government-generated deposits to the QE-time mix.

It is ironic that we had to go through QE, when the power of loan creation on money supply started to wane, for us to truly acknowledge their significance in the process of money creation in the first place. Loans create deposits – yes. But under QE, if Fed buys from a non-bank, the proceeds go in a deposit at a bank without the corresponding increase in loans. If it buys from a bank, reserves at the Fed go up.

Things get more complicated when the government hands out free cash as it also goes on a deposit (Government-generated deposits) with no corresponding loan creation.

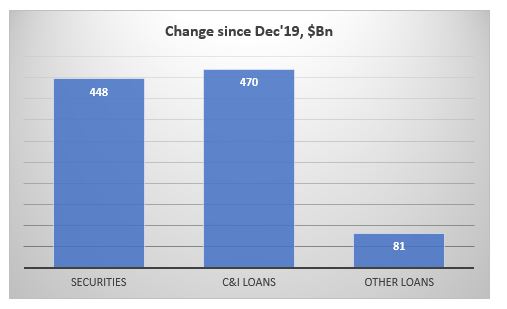

Of those bank credits, actually, only about half are loans, the other half are securities. So, in fact loans have created only about 1/6 of the money supply YTD (would be even less if measured after the Fed/Treasury initiated their programs in March).

What about inflation? Difficult to see how this massive rise of money supply can produce any meaningful push in inflation given that the majority of that cash is simply being saved/invested in the market rather than consumed.

Moreover, this crisis is hitting the service sector much more than any other crisis in the past. And unlike the manufacturing sector, which tends to be more cyclical, this decline in services may be structural as the virus changes our consumer preferences in general, but also in light of the new social distancing requirements. Some of these services are never coming back. This is deflationary, or at minimum it is dis-inflationary overall for the economy.

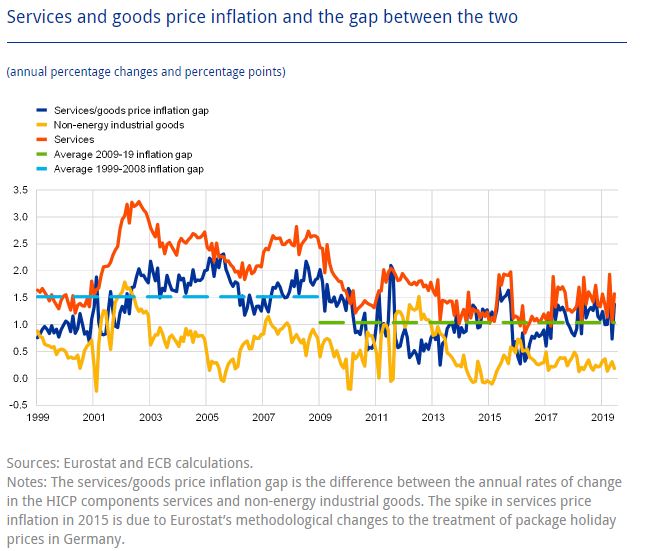

Services price inflation tends to be much higher than manufacturing price inflation. This paper from the ECB has documented that this is a feature for both EU and US economy and has been prevalent for the past 20 years.

However, as the paper demonstrates, the gap between the services and good price inflation has been narrowing recently, starting with the 2008 crisis. I believe that after the Covid crisis, the gap may even disappear completely.

For a sustained rise in inflation, we need a ‘permanent’ rise in free government handouts as that would increase the chance of some of it eventually hitting the real economy. Reality is that, even if this happens, the output gap is so big that inflation may take a lot longer to materialize than people expect. However, anything that shrinks the supply side of the economy (supply chains breakdown, regulations, natural disasters, social disorder, etc.) would have a much bigger and direct effect on inflation.

Bottom line is, as the speed of technological advances accelerates, and with no barriers to that, inflation in the 21st century becomes much more a supply-side than a demand-side (monetary) phenomenon.

Great post, as always. Thanks for sharing!

Isn’t COVID-19 just such a disruption to the supply side of the economy? Disruptions to supply chains, availability of goods, rising move to close borders etc.

Also, isn’t Napier’s point that the US gov will enact more ambitious 1970s style financial repression (as he defines it – through capital controls etc) to punish saving and get some of those reserves into the real economy? His prediction seems to be more of a historical/political one as much as economic.

If gov debt levels keep rising, then the two solutions seem to be raising taxes (deflationary) or pushing inflation up. Haven’t politicians generally preferred the latter? Given the current global mood can’t imagine raising taxes are an option.

Although Napier seems way too aggressive in his timeline – 4 per cent before the end of the year was the last number I heard him mention (!).

Pingback: The normal interest rate | BeyondOverton