The stock market is a forward discounting mechanism.

How much forward?

It seems quite a lot judging by this chart above.

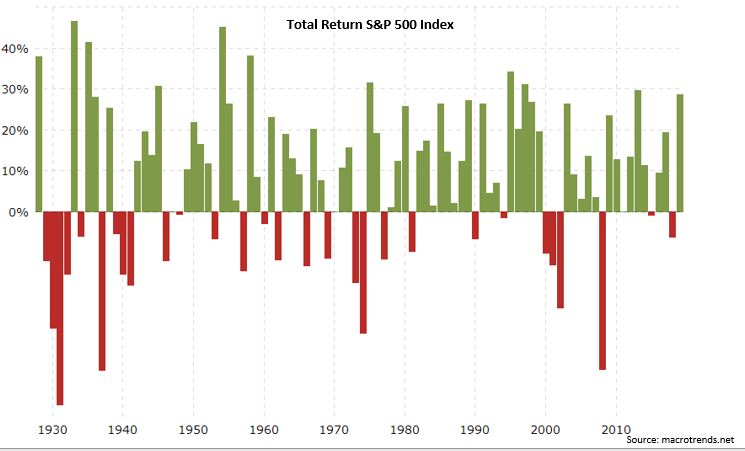

At 28.6% return YTD, the S&P Index is on course to one of its best years on record. Going back to 1927, only 10 years have seen more than 30% returns. It will also wrap up a spectacular decade for the index: with still a few days left in 2019, it can still beat 2013, the best year of this past decade, which finished just shy of 30%, at 29.6%.

While US corporate profits have remained flat since 2012, the S&P Index has doubled. That’s a lot of discounting. But that pales in comparisons to Apple’s share price which has doubled from the lows this year, while its revenue is down during that period (latest numbers for Apple are only as of Q3, so things may change with Q4 numbers released).

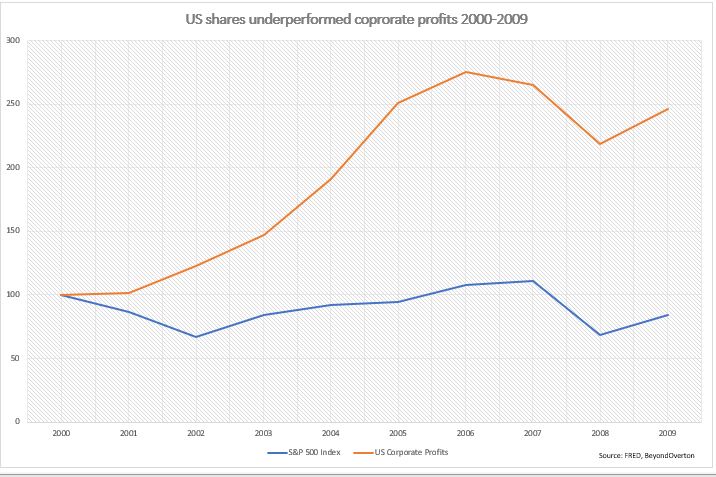

To be fair, the spectacular performance of US stocks this last decade may be just catching up with the previous decade (2000-2009) during which S&P 500 Index declined while US corporate profits increased 2.5x. So, starting point matters.

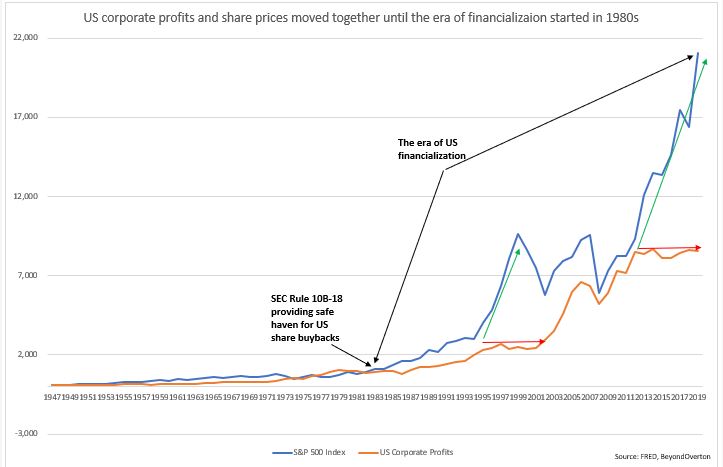

Therefore, it is best to look at the long term-chart, at the beginning of the post, going back to 1947. S&P Index and US corporate profits moved hand in hand until the early 1980s when US financialization kicked in (shareholders primacy and the share buybacks era). There had been, of course, some going back and forth between the two even before 1980 but at the beginning of the 1980s they were ‘on top of each other’.

The volatility between the two sharply increased thereafter. Stocks raced higher and while corporate profits also grew, the growth rate of the S&P index outperformed. Then in the mid-1990s, corporate profits stopped growing but the S&P index continued to race higher. The dotcom crisis and the 2008 financial crisis served as a reset but it still took until 2012 for US corporate profits to ‘catch up’ to US stocks.

The time post 2012 seems very similar to the 1995-2000 period whereby corporate profits did not grow but US stocks rose nevertheless. Only this time, at the end of 2019, the disconnect between the two seems to be the most extreme ever.

The stock market is a forward discounting mechanism indeed, but judging from history a reset is more likely to ‘justify’ that discounting. One problem though: no one can claim to know when that will happen.