…is (actually) Chinese bonds

When speaking to investors, the two most common questions I get asked, given rather extreme levels and valuations of (most) asset classes, are:

1.Should my asset allocation change dramatically going forward? and

2.What is the best risk diversifier for my portfolio?

I have previously opined on this here. Very broadly speaking, on the equity portion, one should reduce exposure to US equities and increase allocation to EM equities (unhedged). On the fixed income side, one should move completely out of the long end of UST and put everything into T-Bills to 2yr UST; exposure to EU-denominated sovereigns should also be reduced to zero at the expense of EM local (unhedged) and hard currency bonds. In the normally ‘Others’ section of the portfolio, one should include soft commodities (or alternatively, scale everything down to make space for them). Finally, in terms of FX exposure, apart from EM currencies through the unhedged portions of the bonds and equities allocations, one should hedge the USD exposure with EUR.

Here I am adding some more general thoughts on what I consider to be the best portfolio diversifier for the next 5 years, possibly even longer. To my knowledge, ‘noone’ is invested in any meaningful way in Chinese bonds (I am excluding the special situations credit funds, some of which I know to be very active in the Chinese credit space – but even they are not looking at Chinese government or bank policy bonds).

The big fixed income funds, the pension/mutual funds, the insurance companies have zero allocation to Chinese bonds. Some of the index followers started dipping their foot in the space but most of them are either ignoring China’s weight or are massively underweight the respective index. Finally, a sign of how unloved this market is, on the passive/ETF side, the biggest fund is just a bit more than $100mm.

Let me just say here that we are talking about the third (possibly even the second, by the end of this year) largest fixed income market in the world. And no one is in it?

Chinese bonds merit a rather significant place in investors’ portfolios. They offer diversification thanks to their low correlation and superior volatility-adjusted return relative to other developed and emerging markets. In addition, Chinese bonds are likely to benefit significantly from both the passive and active flows going forward: I expect up $3 trillion of foreign inflows over the next decade on the back of indexation.

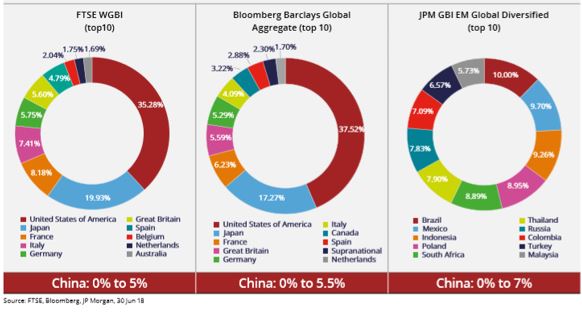

Bloomberg Barclays Global Aggregate Index (BBGAI) and JP Morgan Global Diversified have already confirmed Chinese bonds inclusion in their respective indices. FTSE Russell WGBI is likely to do that next March. This inclusion is a big deal! It will have huge repercussions on the global bond industry. It is a much more important and far-reaching development than a similar inclusion of Chinese equities in global indices last year. And the market is not only not ready for this, but it is also underestimating its impact overall.

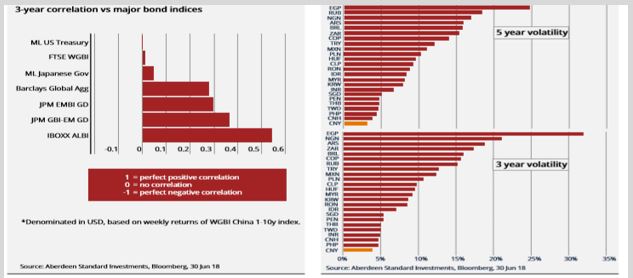

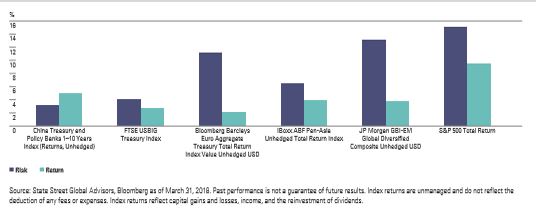

China is a highly rated sovereign with a much better risk/return profile than other high-quality alternatives. Chinese bonds offer a significant scope for portfolio diversification because they have very low correlation to global interest rates which means lower return volatility.

Therefore, China sovereign bonds offer a much better volatility-adjusted return than Global Bonds, EM Hard Currency and Corporate Bonds, US HY and Equities, Global Equities and Real Estate.

Among the plethora of negatively yielding sovereign bonds, China sovereigns offer a good pick-up over other DM bonds while yielding not too much lower than EM bonds. In addition, they offer much more opportunity for alpha generation than both DM or EM sovereign bonds. This alpha partially comes from the fact that Chinese fixed income market is still not so well developed and partially from the fact that there are not many sophisticated foreign players in it, as access to it is still not that straightforward.

However, things are rapidly improving on the access side. Bond Connect has already started to revolutionize the onshore market. Before the setting-up of CIBM, and especially Bond Connect in 2017, access to the China bond market was extremely cumbersome through a lengthy process requiring approvals from high authority (QFII and RQFII). Bond Connect, on the other hand, does not require domestic account and custody while following international trading practices. In addition, not long ago, it started real-time settlement and block trading. As a result, Bond Connect volumes doubled.

Moreover, in September this year, SAFE decided to scrap the quota restrictions on both QFII and RQFII, while Euroclear signed a memorandum of understanding with the China Central Depository & Clearing to provide cross-border services to further support the evolution of CIBM. That opens up the path for Chinese bonds to be used as collateral in international markets (eventually to become euro-clearable), even as part of banks’ HQLA. Such developments are bound to make access to the Chinese bond market much easier for overseas investors.

September proved to be a very important month for the China bond market also because the authorities finally delivered on the interest rate reform agenda. The central bank eliminated the benchmark policy loan and deposit rates in favor of a more flexible reference rate. This should be positive for yield curve formation and the continued expansion of interbank liquidity.

China does not have some of the weaknesses typical of emerging markets. On the opposite, it has very little sovereign FX debt, has large FX reserves, and it is a net creditor to the world. Moreover, some of the foreign debt is most likely offset by foreign assets.

Corporate-sector leverage, however, is still high, though default rates, despite lots of recent media focus, are still relatively low. On the other hand, the recovery rates are high, while the official, banking and household sectors are in relatively strong position which, reflects degrees of freedom to deal with these challenges. China has large amounts of debt with implicit state backing and a culture averse to defaults. In effect, the government controls both the asset and the liability side of the domestic debt issue thus a debt crisis is much less likely than in a fully free-market economy. The fact that China has the ‘fiscal’ space to deal with the private debt issue is one big advantage it has over DM countries with similarly high private debt burdens but which have also already used the option of shifting that debt to the government balance sheet.

The high debt issue and the authorities’ attitude to it, the structure of the economy (export-driven) as well as the potential transition from an extremely high growth rate to a more ‘normal’ one, makes China’s situation very similar to Japan’s in the late 1980s. Yet, there are also major differences. China’s urbanization rate is much below Japan’s before the 1990 crisis, the real estate bubble is only in the top tier cities as opposed to country-wide as in Japan, the Renminbi is more likely to depreciate going forward than massively appreciate which is what happened to the Yen after the Plaza accord.

The high debt issue is a problem China shares not only with Japan but also with most advanced countries in the world. Similar to them, China is fully sovereign (the government has full control of the overall economy balance sheet; the currency peg is a “question mark”, not a real issue given China’s large positive NIIP). Of all these advanced economies with similarly high non-financial debt to GDP, only China has not reached the zero-bound*. It is, therefore, likely for the Chinese policy rate to continue to move lower until it eventually hits 0%.

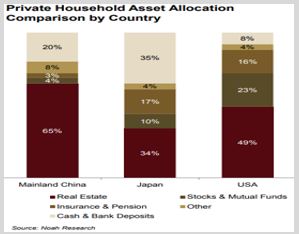

Similar to Japan, it has a high household savings rate and a rapidly ageing population. Yet, Chinese households have relatively low exposure to financial assets and especially to bonds. Given the policy agenda of financial market reform and the life-cycle savings behavior (i.e. risk-aversion increases with age), Chinese households’ allocation to bonds is bound to increase manifold. Moreover, with the looming of the property tax law (sometime next year), I expect the flow into bonds to start fairly soon.

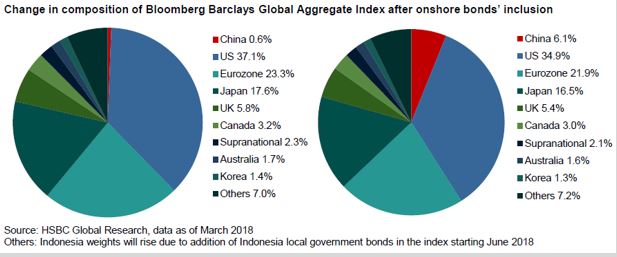

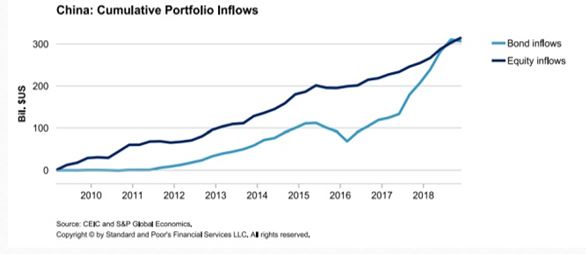

This flow aspect makes the case for investing into China bonds much stronger. Given the size of the Chinese fixed income market, its rapid growth rate and the reforms undertaken most recently, global bond indices had ignored Chinese bonds for too long. However, last year BBGAI announced that it would include China in its index as of April 1, 2019. Purely as a result of this, China bond inflow is expected to reach $500Bn by 2021 as the weights gradually increase from 0.6% to 6%. By then China will be the 4th largest component in the index (after US, Japan and France – and bigger than Germany!)

Before BBGAI’s inclusion, there had never been a bond market that large, that was not included in an index, as the Chinese bond market. In fact, China already represents the third largest bond market in the world, growing from $1.6 trillion in 2008 to over $11 trillion now.

Despite the setback of FTSE Russell postponing its decision to include Chinese bonds into its index to March next year, JP Morgan did follow through with the inclusion. The FTSE Russell decision to wait for the inclusion happened literally a day before Trump announced that he is considering banning all investments into China on the back of the escalating trade war. Tensions since then have been substantially reduced and I do not expect Trump’s warning to materialize regardless. I expect foreign flows into Chinese bonds, therefore, to continue to grow substantially (probably by another $150Bn combined on the back of the FTSE/JP Morgan inclusions).

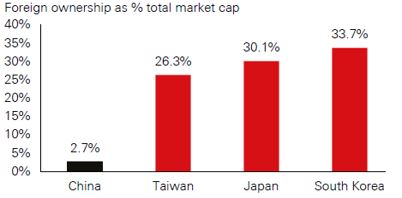

And even after these inflows, China bonds are still likely to remain relatively under-owned by foreigners as they would represent just 5% of China’s total bond market (currently foreign ownership of the overall bond market is around 3%, PBOC expects it to reach 15%). Foreign ownership of China sovereign bonds (CGBs) is slightly higher, but even at around 6%, it is materially lower than in other major sovereign bond markets. This under-ownership is even more pronounced relative to the emerging market (EM) universe (the ranges there are between 10% and 50%).

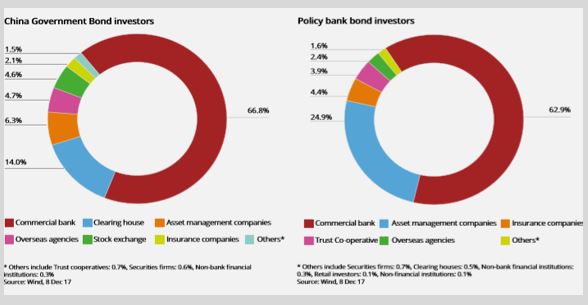

Compare this potential foreign involvement in Chinese bonds with those in Japanese bonds (the second largest market currently in the world, one which, actually, China is likely to surpass very soon): 40% of the traded volumes there are by foreign entities. Foreigners own about 13% of the market there – this may indeed seem small but it is still larger than local banks ownership, plus one has to take into consideration that Bank of Japan owns majority of the issues. The Chinese bond market, on the other hand, is completely dominated by domestic institutions (more than two-thirds is owned by commercial banks).

Finally, foreign investors are expected to continue to get very favorable treatment from the Chinese authorities. The government has an incentive to make things easier as they need the foreign inflows to balance the potential domestic outflows once the current account is liberalized. For example, the tax changes implemented last year allowed foreigners to waive the withholding tax and VAT on bond interest income for a period of three years.

I am still frankly shocked how little time investors have to discuss these developments above but, at the same time, how eager they are to discuss the Chinese economy and the trade tensions. From one hand, they acknowledge the importance of China for their investment portfolio, but on the other, they continue to ignore the elephant in the room being the Chinese bond market. I understand that this choice is perhaps driven by investors’ inherent negative bias towards any Chinese asset, but the situation between asset and asset is much more nuanced.

In the fixed income space, one can be bearish select corporate credit and bullish CGBs or bank policy bonds (in fact, the more bearish one is on corporate credit, the more bullish sovereign bonds one should be). Finally, I do acknowledge that the big unknown here is the currency. But even there, the market has become much more sophisticated: one can now use a much longer CNY/CNH forward curve to hedge.

Bottom line is that if you are still looking for a fixed income alternative to diversify your portfolio and you are not looking at Chinese sovereign bonds as an alternative, you are not being fiduciary responsible.

*For more details, see JP Morgan’s economics research note, “China’s debt: How will it evolve?”