Tags

I don’t think the stock market bulls appreciate the wave of supply that may hit the market in 2019. I know we got used to billions of dollars of share buybacks on the demand side while not paying that much attention to the supply side. Yet, IPOs in the last few years have been quietly building up. In fact, if the experts are right, 2019 could beat the IPO record issuance reached before the dotcom bust.

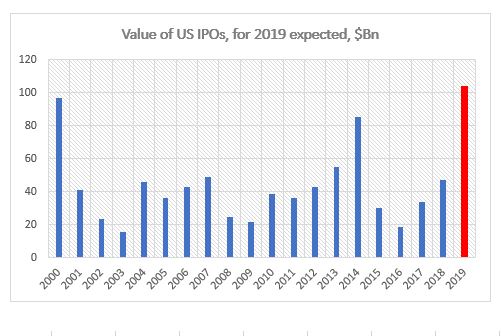

According to Renaissance Capital, the total value of private companies that are planning to go public in 2019 is $697Bn. They estimate that if just 15% of that value exits at IPO, that would amount to over $100Bn which would be more than the record for IPOs set in 2000.

If companies manage to get their valuations just from tech names, there is a minimum of $200bn of value in the pipeline (Lyft, Uber, AirBnb, Pinterest, Slack, Postmates). Using the 15% benchmark, see above, that would make tech IPO size in 2019 somewhat similar to 2018 when the tech sector raised $32Bn in IPOs. But the $200Bn amount is on the conservative side. That would still make the tech sector the largest one in terms of IPO issuance.

How will that play out? Will there be enough demand to offset this supply? With fewer individual retail accounts and fewer active managers than in 2000, how would passive investors react to this?

On top of that, we have the threat of more regulation, especially on the tech sector, but also on the general market with the spectre of a ban on share buybacks looming on the horizon.

Just looking at the supply – demand dynamics, it feels like we do not even need to bother with the ‘subjective fact’ of excessively high valuations and recent earnings downgrades to make a good bear case for US stocks. But I can already foresee what the bulls would say, “If you discount the data by market cap, the extreme IPO number does not look that bad”. I guess, the jury on this is still out.