Tags

There seem to be three aspects of the recent debate about China’s private credit build-up:

1) Is it excessive? Yes, but it is not extreme.

2) Has it been misallocated? Probably yes, but not necessarily more than in other countries now or in earlier stages of development.

3) How will the authorities handle the inevitable credit burst? That remains to be seen, but due to its unique political system, China seems to be more in control than other countries which have undergone a similar fate Question is whether this control will result in a positive outcome.

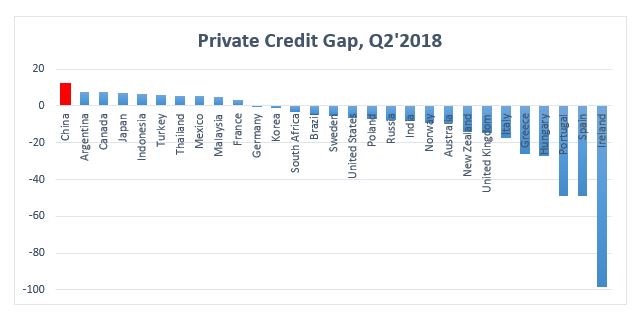

China’s recent credit build-up is indeed big: its recent private credit-to-GDP gap (a BIS indicator measuring the speed of credit creation now relative to its long-term trend) is currently the largest in the world.

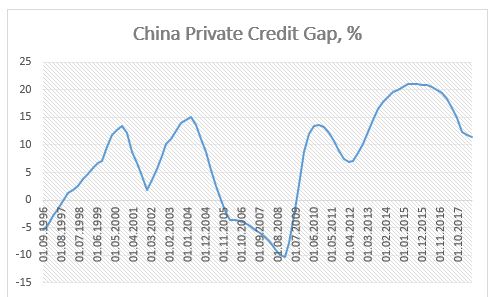

China’s credit build-up seems to have accelerated especially so after the great financial crisis in 2008.

However, private credit creation growth in China reached a top (using four quarters MA of the credit gap as an indicator) sometimes in 2015 and has been decreasing since then.

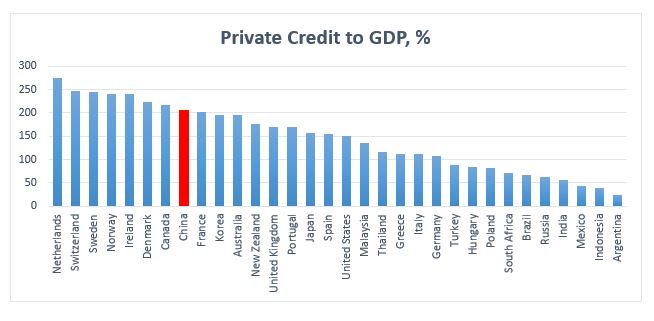

Indeed, China’s absolute private credit to GDP ratio is nowhere near some other countries’ extremes.

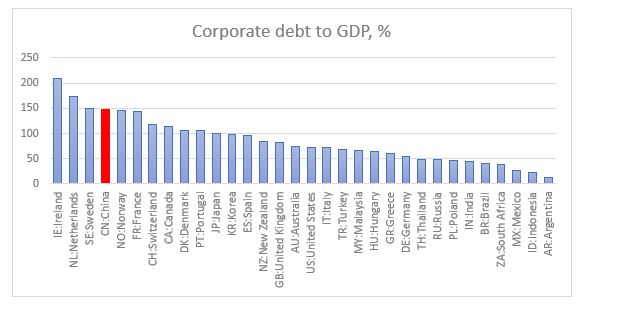

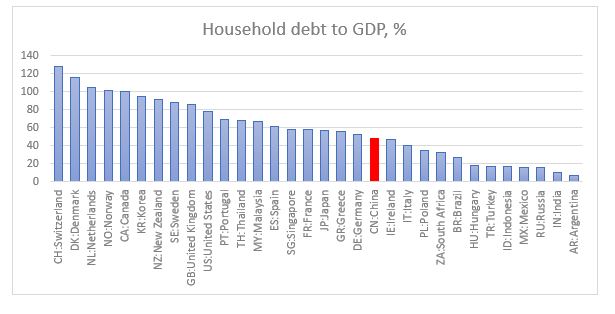

It is the corporate sector which has levered…

…with households still relatively unlevered.

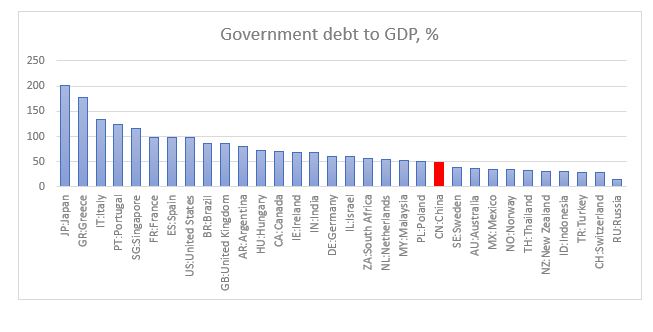

And of the corporate sector, most of the debt is concentrated in the SOEs. Finally, its government sector is unlevered, leaving the total (private + public) credit to GDP even lower relative to majority of other countries.

Bottom line is, China seems to have a lot of credit space left, giving it some room for “a beautiful deleveraging”.

The fact that most of the credit is in CNY gives a lot of flexibility of how that deleveraging is done – on China’s own terms (there is some foreign currency debt but a lot of it is either matched by corporate foreign currency assets or covered by the country’s own FX reserves).

Having travelled extensively throughout the whole country, I can confirm that there are ghost cities but the state of the overall infrastructure, pretty much everywhere, is first class, probably on par, or even better than most of continental Europe while putting US/UK infrastructure to shame. Having travelled also through all of Central Asia and after spending a month in the Philippines and now in Malaysia, I can also attest that the alternative, not spending so much on infrastructure, is infinitely worse.

So, by investing in real estate and infrastructure projects, and given its large population which is emerging from decades of under-development, is China misallocating more capital relative to:

- the developed world, particularly, UK and US, where since the 1980s majority of credit created was against existing (unproductive) assets like residential real estate and financial assets for speculative purposes, leaving current infrastructure in a crumbling state? That’s in sharp contrast to the period between WW2 and the 1980s when credit was allocated to the production of goods and services and infrastructure projects like the interstate highway system in the US (a period more comparative to China’s developments now, and one largely heralded as the golden stage of economic growth).

- the developing world, which similar to China now is also in need of massive infrastructure development but instead national capital has been syphoned off to offshore wealth centres? Yes, there has been private capital outflow from China as well but it would have been much bigger had the capital account not remained closed.

It would take time before we know for sure whether the decisions Chinese leaders are making are beneficial for the country or not. It is fairly likely, though, that this credit expansion is not sustainable. Should this boom be followed by a bust, we could be fairly certain that the situation would be carefully managed by the authorities, unhindered by either hostile domestic political opposition, like in the majority of the democratic Western world or by foreign creditors, like in the majority of the developing world.

How would they handle it? If history is any guide, they did a pretty good job both during the Asian crisis in 1997/98 and the great financial crisis of 2008. Third time lucky?

I expect the authorities to continue building up the social safety net – pension and health care system – alongside expanding and improving the financial assets universe. They could simultaneously deflate the real estate bubble, by starving it of additional capital and inflate financial assets by encouraging diversification into them. Unlike, developed world countries where household wealth generally collapses during crises, Chinese households could come out unscathed from this as they are unlevered. In addition, any losses on their real estate portfolio could be offset by gains in their financial assets portfolio. Finally, with the right social safety net in place, they would also feel more secure for their future than before and therefore welcome such an outcome.

Note: All data used above is from BIS