Tags

- People have been proposing a variety of reasons for the LIBOR-OIS spread continued widening. And majority of them make sense. My view is that we cannot discard the fact that the gradual replacement of Libor with the Secured Overnight Financing Rate (SOFR) is also playing a major role.

- Unless you are actually directly involved in the Libor market, and there are only a ‘handful’ people left in it now, the larger investment community is not paying enough attention to these changes.

- At the moment there are four eligible benchmark interest rates which can be used for hedge accounting purposes, as per FASB: UST, LIBOR, OIS (based on FFER), SIFMA Municipal Swap Rate. The Fed has requested that the OIS based on SFOR to be added to the list.

- This is a big deal. There are $350Tn of worth of loan/bonds, etc. tied to Libor. And by 2021 Libor will be gone. From April 3, 2018, the Fed will start publishing Libor’s replacement, SOFR. Anyone involved in the Fixed Income markets better start to get ready.

Of course, LIBOR may remain viable well past 2021, but we do not think that market participants can safely assume that it will. Users of LIBOR must now take in to account the risk that it may not always be published.

Jerome H. Powell, Roundtable of the Alternative Reference Rates Committee, November 2, 2017

- The meaning of Libor may still be the same, but the significance of the way it is derived, has massively changed since the scandals of 2012, and now its relevance is about to fade: Libor is no longer reliable.

In our view, it would not be feasible to produce a robust, transaction-based rate constructed from the activity in wholesale unsecured funding markets. A transactions-based rate from this market would be fairly easy to manipulate given such a thin level of activity, and the rate itself would likely be quite volatile. Thus, LIBOR seems consigned to rely primarily on some form of expert judgment rather than direct transactions.

Jerome H. Powell, Roundtable of the Alternative Reference Rates Committee, November 2, 2017

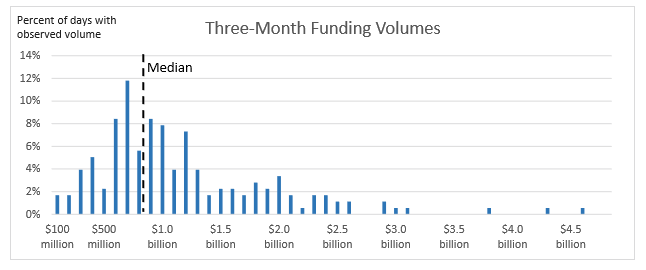

- Today, there are 17 banks that submit quotes in support of Libor. Look at the distribution of daily aggregate wholesale dollar funding volumes for the 30 global systemically important banks: the median is less than $1 billion per day. On some days, there are less than $100 million.

- SOFR is very different. To begin with, it is secured (UST collateral), it is only O/N and it is only transactional but volumes are massive (see below). Libor is unsecured, term and it is both transactional and ‘estimated’ (increasingly more the latter). SOFR is kind of a ‘pure’ GC rate.

- SOFR is a good proxy for a risk-free rate. It could offer the broadest measure of dealers’ cost of financing Treasury securities O/N and, therefore, it could provide useful information regarding O/N demand and supply for funding in the UST repo market.

- So, the market has three years or so to start converting $trillions worth of contracts which point now to Libor, to SOFR (some of them will just expire before that date). The problem is, because Libor is much higher than SFOR, the receiver of Libor on a legacy contract will require compensation in order to agree to the conversion.

- There are just too many issues with this conversion. For example, how do you deal with current Libor contract which requires payments based on 3m Libor after the introduction of SFOR which is only O/N (CME will start trading future on SOFR in May)?

Now, however, market participants have realized that they may need to more seriously consider transitioning other products away from LIBOR, and the ARRC has expanded its work to help ensure that this can be done in a coordinated way that avoids unnecessary disruptions.

Jerome H. Powell, Roundtable of the Alternative Reference Rates Committee, November 2, 2017

- When you need to settle floating rate coupons then you need to use OIS (based on SOFR), but there may not be that much (term) liquidity there at the beginning. You don’t want to be relying on this then if you are going to be converting trillion of $ of Libor.

- Darrell Duffie proposes instead an auction and protocol based approach. Bottom line is that the LIBOR->SFOR conversion is a big thing in the markets and unless you dig in regulatory/compliance documents, very few people are discussing it.