I would not be blindfolded by the fact that the US is trying to go back to ‘normal’ with the Fed on a rate-raising spree. ‘Normal’ changed a long time before 2008. You cannot go back to ‘normal’ with a broken monetary transmission mechanism. We can create all the money in the world but if it goes in the hands of the few, if it is subsequently ‘hoarded’ and if it cannot reach the end consumer because Work≠Job≠Income (whether that is because of technology, globalization or whatever) or because the credit channel is closed (the end of the private debt super-cycle in 2008), the economy is not going to go anywhere. And if there is little demand because there are not enough mediums of exchange, aka money, circulating in the economy, optimizing production is a waste of time and resources.

Instead of focusing on going back to a ‘normal’ interest rate policy, a forward-looking central bank would be looking into the opportunity presented by the rise of the blockchain technology and the subsequent spread of digital cryptocurrencies. The latter are a direct response to the broken down monetary transmission mechanism: if the traditional mediums of exchange do not circulate in the economy, people are devising their own ways of exchanging goods and services.

The interest-rate cycle is something of the past now. If the financial crisis of 2008 did not make it obvious, perhaps, we have to wait for the next one, which would be here like clockwork as policy makers embark on the policy of ‘normalization’. But there is some hope that some central banks are looking into ways to introduce a digital currency of their own and opening their balance sheet to the public at large.

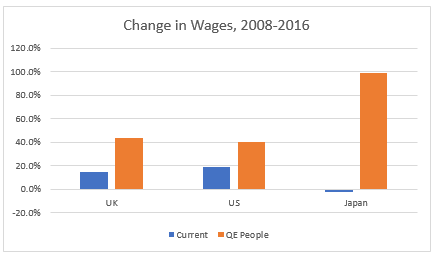

Back of the envelope calculation shows that if the money spent on buying financial assets by the central banks of UK, US and Japan, was instead disbursed directly to the people, working wages would have risen substantially.

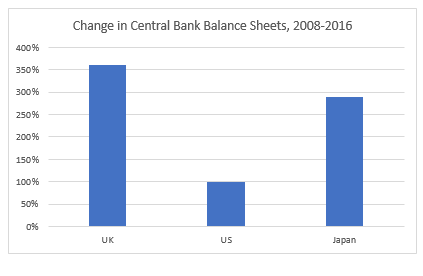

Between 2008 and 2016, central banks’ balance sheets have risen by 360% in the UK, 99% in the US and 280% in Japan.

Source: Bank of England, US Federal Reserve, Bank of Japan

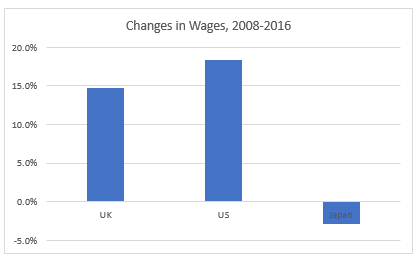

At the same time, over this period, nominal wages have risen by only 14.8% in the UK, 18.4% in the US and actually fallen by 2.9% in Japan! In 2016, the average annual wage in the UK was GBP 34,142, in the US – USD 60,154 and in Japan – Yen 4,425,380.

Source: OECD

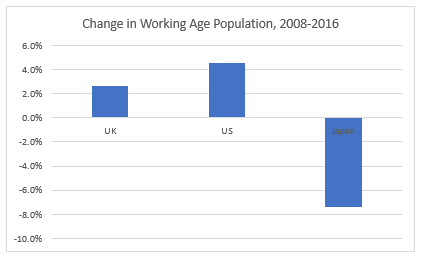

Japan is peculiar also because its working age population declined by 7.4%, while US’ and UK’s rose by 4.5% and 2.7%, respectively, during this period.

Source: OECD

I took the actual change in central bank balance sheets and divided it over the average working age population between 2008 and 2016. If this money could have been disbursed directly to the people, workers would have received a lump sum of GBP8,574, USD10,997, Yen4,430,424 over the period.

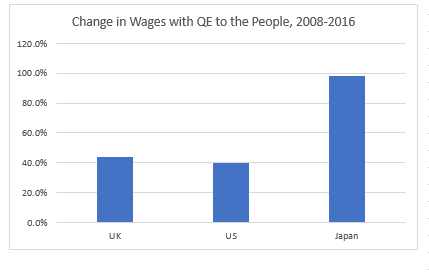

Let’s imagine that this lump sum was disbursed to the working age population at the end of 2016. Compared to 2008, their wages in 2016 would then have been higher by 44% (UK), 40% (US), 98% (Japan)!

If wages could indeed ‘miraculously’ rise by almost half in the UK and US and almost double in Japan over this 8 year period, what are the chances that we would still be stuck around 2% inflation in the US and UK and around 0% in Japan? Where would GDP be?

This is a very simple exercise. Undoubtedly real life is much more complicated that this and it is rarely black and white. Moreover, this would have been a lump sum disbursement, a one-off boost to income, and not a permanent rise in wages. Consumer behavior in this case, Ricardian equivalence, etc., would have been very different from a situation with a permanent rise in wages.

However, instead of patting ourselves on the back that things could have been much worse had the central banks not backstopped the financial system by buying financial assets, can we not also think how they could have also been much better if we found a better use for the money miraculously created out of thin air? If we could create money out of thin air to boost financial asset prices, is it really not possible to devise a way whereby the consumer also gets a permanent rise in income? Can we have an adult conversation about the effects of such an experiment without resorting to the taboos of the past? Can we include people other than economists in this conversation?

The free market may be the best and most efficient optimization model available so far to us, but what if we are optimizing the wrong variable?