Source: Z1 Flow of Funds, US Federal Reserve/Click to enlarge

“For an individual agent, additional income is necessarily accumulated in financial or real assets. The income not spent (the individual’s “saving”), which is initially received in the form of additional settlement medium, is allocated across asset classes. But for the economy as a whole this is obviously not true. The allocation of savings simply represents a gross transfer of assets across individuals: the increase in deposits of income receivers is matched by the decline in deposits of those that pay that income out. It is only when the additional income is supported by issuance of financial claims (eg credit or shares) that financial assets and liabilities are created. By the same token, the popular and powerful image that additional saving bids up financial asset prices (and hence depresses yields and interest rates) because it “has to be allocated somewhere” is misleading. There is no such thing as a “wall of saving” in the aggregate. Saving is not a wall, but a “hole” in aggregate spending.” BIS Working Paper 346

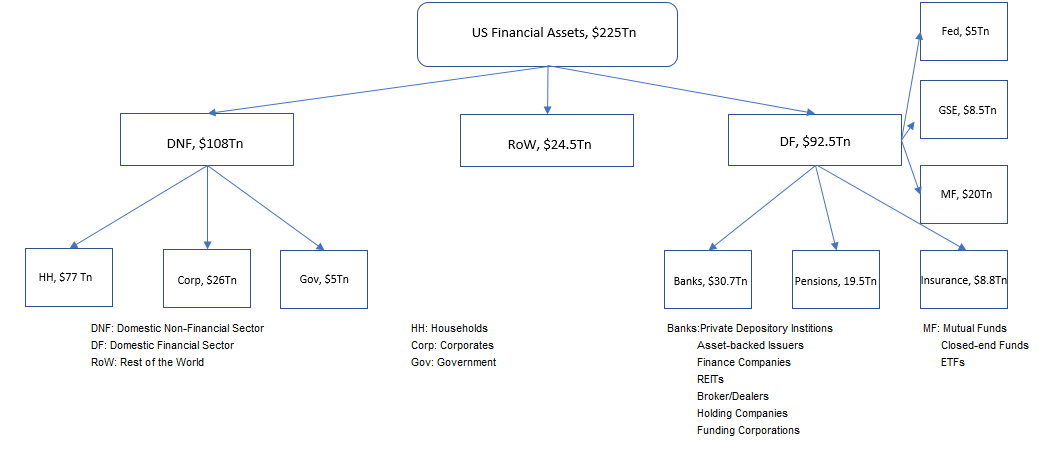

- There are $225Tn of US financial assets in terms of market value (Chart above).

- Financial assets growth started to surpass GDP growth in the early 1980s as the financialization of the US economy began. For example, for 40 years between 1945 and 1985, the ratio of financial assets to GDP varied between 5x and 6x. After 1985, the ratio started moving higher and higher and currently stands at record 12x!

Source: Z1 Flow of Funds, US Federal Reserve

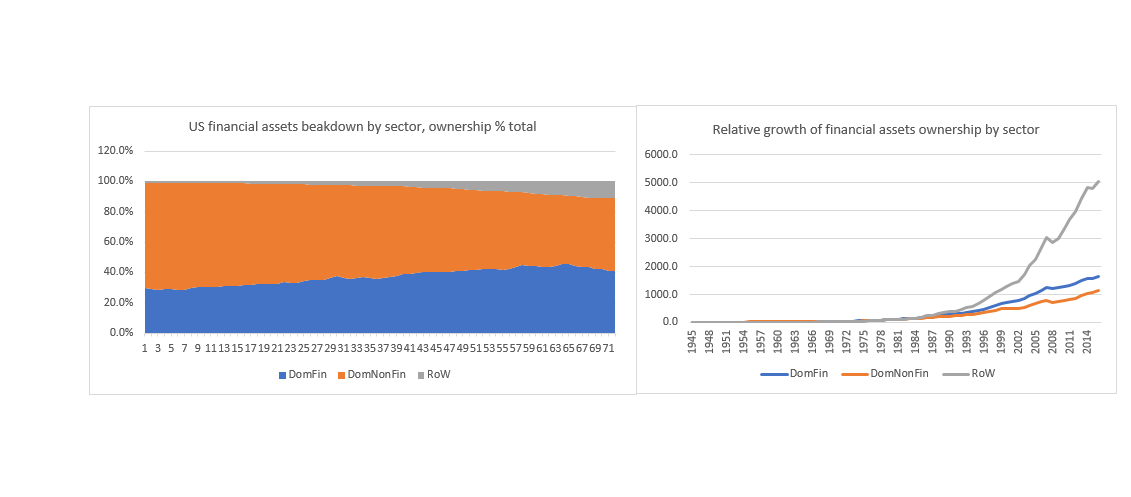

- In terms of ownership, financial assets are split among three major sectors: Domestic Non-Financial, Domestic Financial and Rest of the World.

- The Domestic Financial Sector started gathering more and more financial assets relative to the Domestic Non-Financial Sector in the early 1990s. But it is really foreigners who began heavily investing in the US as trade flows picked up in the late 1990s and strong globalization trends emerged.

Source: Z1 Flow of Funds, US Federal Reserve/Click to enlarge

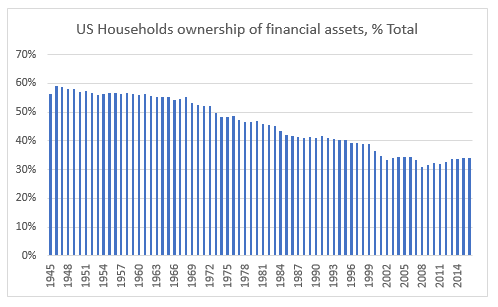

- US households’ direct ownership of financial assets has gradually decreased since 1945 in line with the financialization of the US economy. As absolute savings increased, the financial industry expanded to meet households demand for new products in which to invest them. After the 1980s, the financial industry not only was creating new products but also started investing on behalf of households.

Source: Z1 Flow of Funds, US Federal Reserve

- Savings are a dead weight on the real economy as they drain funds away from it. If instead they were invested in real projects, arguably, employment and economic growth could have been higher. At the moment, it is the financial sector, primarily, which benefits from this surplus capital.

- As this surplus capital gets diverted into savings, new money must be created to serve the real economy. This new money gets created as debt. This has generally been a more efficient method of money creation than most other ones in the past as it matches closely economic activity.

- However, as the debt stock increases mathematically due to positive interest rates, this efficiency decreases. In addition, not only new money must be created to serve the real economy but also to pay back the old debt.

- The financial sector gets a cut on both the asset side of the balance sheet (managing the surplus capital) and on the liability side (creating the debt).

- Looking at the US economy from this sectoral balance point of view, we should be also asking ourselves questions about the role of this surplus capital.

- For example, what is the need for government bonds in a fiat monetary regime? Are they ‘created’ to fund US government budget deficits, for example, or to meet the demand for positively yielding (protection from inflation) and safe (protection from default) assets as the surplus capital increases?

- Given that companies generally prefer to fund themselves using internal capital, what is the role of the stock market especially when there is also surplus corporate capital?

- How far can we go monetizing the real world to create enough financial assets to meet the demand of the increasing capital surplus globally?

- In the increasingly digital world where the marginal cost of production is zero and in the old industrial world where the marginal cost of production is dropping fast because of the advances of technology, how much surplus capital in aggregate do we need?

- Do we have so much surplus capital because our income distribution model is broken?

…